-

-

![Michael Rosen]()

-

CIO Insights are written by Angeles' CIO Michael Rosen

Michael has more than 35 years experience as an institutional portfolio manager, investment strategist, trader and academic.

RSS: CIO Blog | All Media

Economics in Action

Published: 06-12-2017

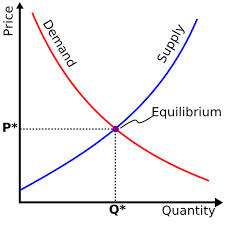

The intersection of supply and demand determines price and quantity: there is no more fundamental principle of economics (see graph below). We rarely see this principle in action because prices for most consumer goods and services change little week-to-week. All that means is the market maintains a constant equilibrium (which is set by the price) of supply and demand: either there is little change in supply or demand, or the changes are very modest, and market forces adjust quickly to maintain that equilibrium.

Commodity prices are much more volatile than consumer goods prices, meaning there are frequent “shocks” either to demand or, more likely, to supply. Scarcity, due to weather, war or other natural or man-made factors, will drive prices higher (the supply curve shifts up to the left in the graph above), and a glut, (a supply curve shift to the right). will pushes prices lower. For many commodities, prices can remain much higher or lower than normal because it takes time for suppliers to react to the change in prices. In the case of agricultural commodities, a season will often have to pass to allow farmers to plant more or less of a crop. In the case of minerals, closing or (especially) opening a mine is a multi-year endeavor. So supply typically acts slowly to prices.

But there’s another possibility: suppliers can adjust their cost curves to align more closely with current prices. There is no better example of this than in the US oil industry.

The graph below contains three data series: the blue area graph shows US oil production, the red line is the spot price of WTI oil, and the green U-shaped line is the number of oil rigs in operation, all over the past five years.

The price of oil (the red line) collapsed in mid-2014, falling from over $90/barrel in June to $35 by January 2016. The high price of oil prior to 2014 encouraged more domestic production, which grew more than 50% from 2012. Production continued to rise for a year after the fall in the price of oil, peaking at more than 9.5 million barrels per day in June 2015. That’s when the rig count begins, and we see it plummet from around 750 in 2015 to about 250 a year later. Production likewise began to fall in mid-2015, dropping by about one million barrels per day by June 2016.

But then something interesting happened. The price of oil had rebounded modestly off its low, but producers stopped shuttering and started to add more rigs. This was not driven by higher prices for oil, which generally stayed in a range of $40-50 per barrel, half the price of just two years before. Why then would companies increase production (supply) when the new equilibrium price was 50% of its prior level? The answer is the industry shifted its cost structure lower.

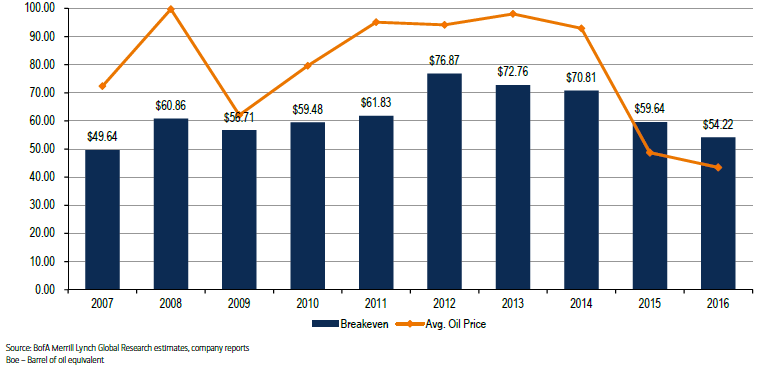

The graph below estimates that the US oil industry lowered its break-even cost by 30%, to about $54/barrel over the past five years. But looking at 2016’s reserve replacement costs (RRCs) of the largest producers, reflecting their actual costs of replacing reserves last year, the industry average break-even price of oil falls to just $42/barrel.

It’s no surprise then that rig counts are up and domestic production is over 9.3 million barrels per day, not far from the recent peak. The industry has successfully shifted its cost curve lower, partly because the oversupply of workers and equipment pushed their costs lower, and partly because of more and better use of more and better technology.

Advances in technology mean the days of wildcatting and dry holes are over, although I’m still inclined to follow the advice of J. Paul Getty. When asked the secret for getting rich, he replied, “Wake up early, work hard, strike oil.” I’ve embraced two of the three; I’m still working on the third.

Print this Article

-

![Puerto Pobre]() 30 Jun, 2015

30 Jun, 2015Puerto Pobre

An honest politician may be oxymoronic (or is just moronic?), or maybe it's the black swan that surprises us when seen. ...

-

![Beach Reading]() 19 Mar, 2026

19 Mar, 2026Beach Reading

We are having a bit of a heat wave here in Southern California, so take your reading to the beach! I have six new ...

-

![Beware Parabolas and Populists]() 13 Jun, 2017

13 Jun, 2017Beware Parabolas and Populists

In scouring the world for investment opportunities, the chart above caught my attention. It shows the year-to-date ...

-