-

-

![Michael Rosen]()

-

CIO Insights are written by Angeles' CIO Michael Rosen

Michael has more than 35 years experience as an institutional portfolio manager, investment strategist, trader and academic.

RSS: CIO Blog | All Media

Two (Percent) is a Sad Number

Published: 09-21-2020

Last month, the Federal Reserve unveiled its new monetary framework, following an intensive 18-month review. The principal change was to abandon a target inflation rate (2%) in favor of an average inflation rate (still 2%). Most observers take this as the Fed communicating that it will not begin to tighten monetary policy even if inflation rises above 2%, but will rather tolerate a higher inflation rate for some time to compensate for the (long) period of inflation below 2%. In practical terms, the Fed expects interest rates to remain at the current very low levels for the foreseeable future (at least until 2023, and probably beyond).

Big deal, you say. Well, maybe so, but inflation and interest rates are pretty important variables in virtually every aspect of the economy. My own 18-day, non-intensive review of this new framework affords the opportunity to share some thoughts on inflation, interest rates and Fed policy.

First, with respect to this policy shift, there is little immediate impact. The Fed has pegged the overnight lending (Fed funds) rate at 0-0.25%, and that doesn’t change. Investors expected policy to remain unchanged for the foreseeable future, and that expectation remains. So, in immediate, practical terms, this is no big deal. But, there is a “but.”

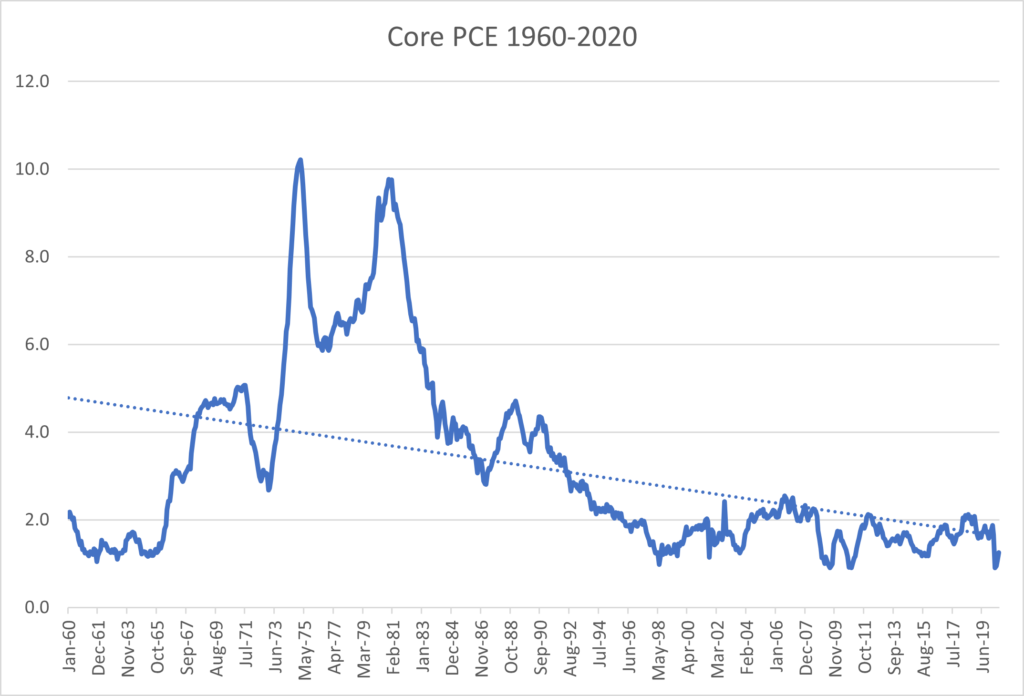

The new framework introduces another level of uncertainty for investors. The Fed will tolerate (even target) an inflation rate in excess of 2% for some time in order that inflation average 2% for some time. But what is some time? The US inflation rate (as measured by the core personal consumption expenditures (PCE), the Fed’s preferred reference), has averaged 1.6% p.a. for the past decade, 1.9% for the past 30 years, 3.2% over the past 60 years (see graph below). What time period will the Fed use to evaluate the average inflation rate? And will it change policy once average inflation finally reaches 2%, or would it prefer to see a period of higher inflation?

Federal Reserve staff tried to clarify the new policy with an obtuse, formula-laden paper (Arias, Jonas, Martin Bodenstein, Hess Chung, Thorsten Drautzburg, and Andrea Raffo (August 2020), “ Alternative strategies: How do they work? How might they help?” Federal Reserve Board Finance and Economics Discussion Series 2020-068) that looks impressive but answers nothing (the key formula is below; it’s not that complicated, but good luck figuring out how it translates to actual monetary policy).

So, while there may be no immediate practical change in monetary policy, should inflation rise above 2%, investors will not be able to know what to expect from the Fed. Should inflation fail to reach 2%, this framework offers no method of addressing that shortfall.

The Fed is signaling that even if the unemployment rate falls to record lows, investors should not expect a tightening of monetary policy. The Fed is saying it will “tolerate” very low unemployment in exchange for rising inflation. For decades, economists, the media and the general public have had a mental model (a formal one in the case of economists, but no truer) that there is an inverse relationship between unemployment and inflation, the so-called Phillips Curve: rising unemployment translates to lower inflation, and higher inflation comes with declining unemployment.

The Phillips Curve was wrong when it was promulgated in 1958. William Phillips, a New Zealand economist at the London School of Economics, wrote a paper on unemployment and wage rates in the UK between 1861 and 1957 that suggested this empirical inverse relationship. A decade later, Milton Friedman and Edmund Phelps refuted the study. Friedman correctly characterized inflation as purely a monetary phenomenon: too much money chasing too few goods. The Phillips Curve has persisted as a working model of the economy because, in the very short-run, a sharp rise in unemployment can lead to an immediate decrease in demand for goods, and thus an oversupply, causing prices to fall. As unemployment falls, spending increases, so goes the theory, as do prices.

The fallacy in the Phillips Curve is that it ignores the great virtue of capitalism, that is, that it is dynamic, and thus able to adjust to changes in demand. If people want to buy more Chevrolets, General Motors will gladly produce more Chevys. If GM raises the price of Chevys, consumers will buy another model, or take the bus. Supply adjusts to demand, with no longer-term impact on the general price level. That can only be affected by too much money circulating in the economy relative to its demand.

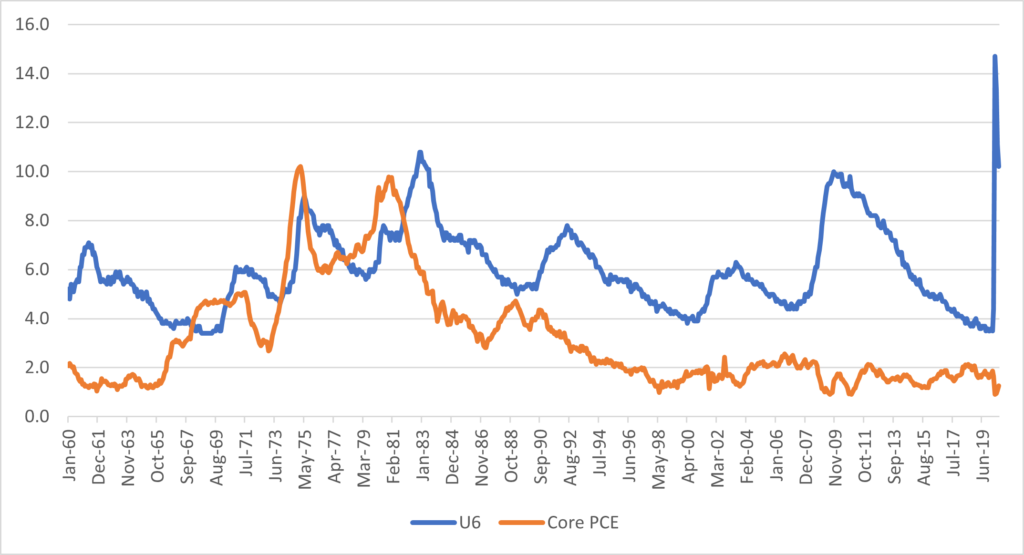

The graph below charts the unemployment rate and the core inflation rate in the US since 1960. There is no correlation between these two series. Actually, its correlation is positive 0.26; not even negative 0.26. This notion that low unemployment signals rising inflation, and vice versa, is simply untrue, yet somehow persists in the general public and in economists’ models. Even in the Fed’s new framework, the Phillips Curve is assumed to exist; the Fed is just not going to be as sensitive to it as in the past. I suppose that’s some progress.

Unemployment Rate and Core Inflation, United States, 1960-2020

So why did the Fed change its monetary framework? My guess is that the Fed is concerned about its policy levers in the next recession. Historically, interest rates were slashed about 5 percentage points in a recession, providing much-needed monetary stimulus to counter the economic contraction. A higher inflation rate would allow the Fed to raise interest rates in order to give them some needed ammunition in the next downturn.

This argument is illogical and ill-considered. The Fed wants higher inflation so that they may justify raising interest rates so that they may then cut interest rates in the next recession. Perhaps that makes sense to someone, but the logic escapes me.

There is a more fundamental problem with this framework: why is 2% the magic inflation number? Inflation is a tax on the purchasing power of money. In other words, inflation erodes the value of money over time. At an inflation rate of 2%, money loses half its value in 36 years. At a 1% inflation rate, the value of money falls by half in 71 years. At an inflation rate of 0%, money retains fully its value. Inflation in the US (again, core PCE) has averaged 1.6% over the past decade, 1.9% over the past 30 years. There is no inflation problem in the US, and certainly not that it’s too low.

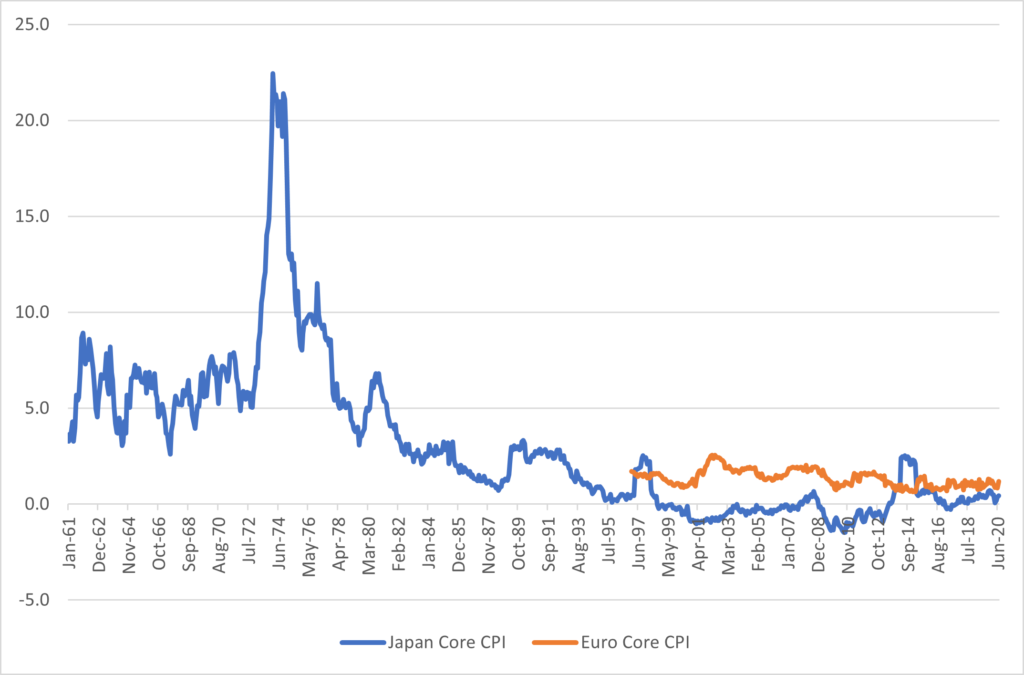

Even if higher inflation were desirable, why does the Fed think it can conjure this rise when other central banks have failed for decades? Core inflation in the Euro area has averaged a little over 1% p.a. for the past 20 years, whereas inflation has been zero in Japan for 30 years (see graph below).

Core Consumer Prices in Japan (1961-2020) and the Euro Area (1997-2020)

Source: OECD

Japan’s experience is instructive, yet has received very little serious consideration by American media or policymakers. Yes, its demographics are ahead of and worse than America’s, although our severe restrictions on immigration mean we are catching up faster to the prospect of a shrinking population. Still, the Bank of Japan (the BOJ, its central bank) has been buying every asset it can find, including a fair chunk of the equity market as well as the majority of every bond the Ministry of Finance pumps out in eye-popping amounts. The result: zero inflation. Inflation is a monetary phenomenon, full stop. Central bank ballooning of balance sheets and purchases of every available financial asset does not cause inflation, as the BOJ has demonstrated. I am perplexed why central bankers think otherwise.

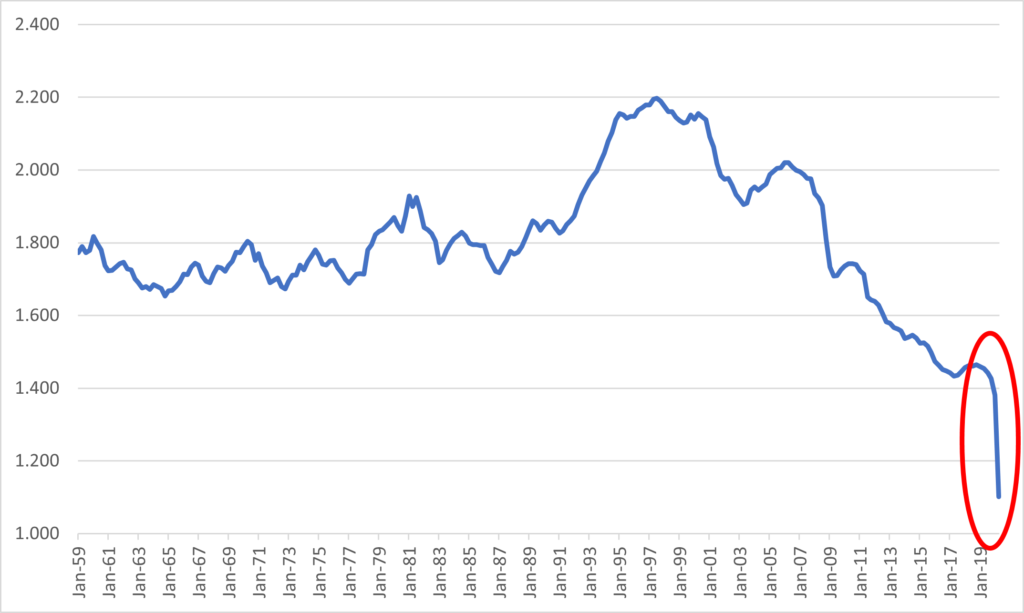

The Fed hasn’t come close to the magnitude of intervention the BOJ has engaged in, but it thinks that it will be able to create higher inflation, how, exactly? The US economy is not running at any supply constraints. Capacity utilization is 71%, but it never exceeded 80% in the past decade. The massive amount of debt we incurred to counter the short-term impact of closing the economy this year will retard growth over the next few decades. Most importantly for inflation is that it cannot rise when money velocity is plunging (see graph below). The Fed, the BOJ, the ECB have all added trillions of dollars (yen and euros) to the ledgers of banks, available to lend to businesses to invest and to households to spend, but businesses and households are doing neither.

Velocity of M2 Money Stock, Quarterly, 1959-2020

Business investment is low and consumer spending is weak because uncertainty is high. When uncertainty is high, the demand for cash is high. Corporate balance sheets are bursting with cash, households have de-levered, and investors are selling stocks and holding cash and bonds. This expresses pessimism and anxiety.

There are powerful deflationary forces in the world: some are structural, some the residual of deflated asset bubbles, and some an expression of risk aversion. In the face of these forces, massive expansion of bank reserves and central banks propping up every asset class has not engendered higher inflation, and will not because that is not what causes inflation to rise. Even more to the point, higher inflation is not desirable. We are left with a policy goal (higher inflation) that is misguided and an approach (asset purchases) that is ineffective. It’s like the old joke about the restaurant who’s food is bad but at least the portions are large.

Policymakers should focus on establishing a consistent framework and supportive environment that encourages business formation and innovation. Inflation expectations should be firmly anchored at zero.

One is the loneliest number (we are told), and two can be as sad as one (it is, after all, the loneliest number since the number one). But zero is best of all. A dynamic, innovative, growing economy with inflation at zero (not one, or two, or higher for some time) should be the goal.

Print this Article

-

![Falling Behind]() 25 Aug, 2016

25 Aug, 2016Falling Behind

It's good to be tall.Tall people tend to be more highly educated, earn more over their careers, are higher in the social ...

-

![Europe Sputters, US Cruises]() 15 Dec, 2014

15 Dec, 2014Europe Sputters, US Cruises

Europe's unemployment rate is 11.5%. Europe is currently growing at less than 1%. A rule of thumb is that it takes ...

-

![Sunrise or Sunset: Thoughts on a Post-Pandemic World (Part 1)]() 27 May, 2020

27 May, 2020Sunrise or Sunset: Thoughts on a Post-Pandemic World (Part 1)

Two and a half months of isolation engenders reflection, on what weve endured, and contemplation on what the future may ...

-