-

-

![Michael Rosen]()

-

CIO Insights are written by Angeles' CIO Michael Rosen

Michael has more than 35 years experience as an institutional portfolio manager, investment strategist, trader and academic.

RSS: CIO Blog | All Media

Everybody Out'ta the Pool

Published: 05-15-2018

Markets work through the forces of demand and supply. This axiom applies to all markets, from housing to marriage (as Gary Becker famously noted), and anywhere there is an exchange of goods or services (or mates). In all markets, price is the regulatory mechanism that ensures an equilibrium between the amount demanded and the amount supplied. Adam Smith called this the “Invisible Hand.”

You knew all this already, because it is about as fundamental a concept in economics as exists. The price of that house is X, or the price of that automobile is Y, because X and Y are the prices that clear the market, that is, that determine that the supply meets the demand. Too many unsold houses or automobiles, and the price will fall to a level that will stimulate demand. Sudden demand for more houses or automobiles, and the price will rise. A falling price signals to cut back production, a rising price tells suppliers to make more. Most of the time, this is exactly how markets “work.” Yet sometimes, we observe market behavior that seems at odds with our expectations, and we scramble to uncover the hidden forces that produce this unexpected behavior. The labor market today has many economists scratching their heads.

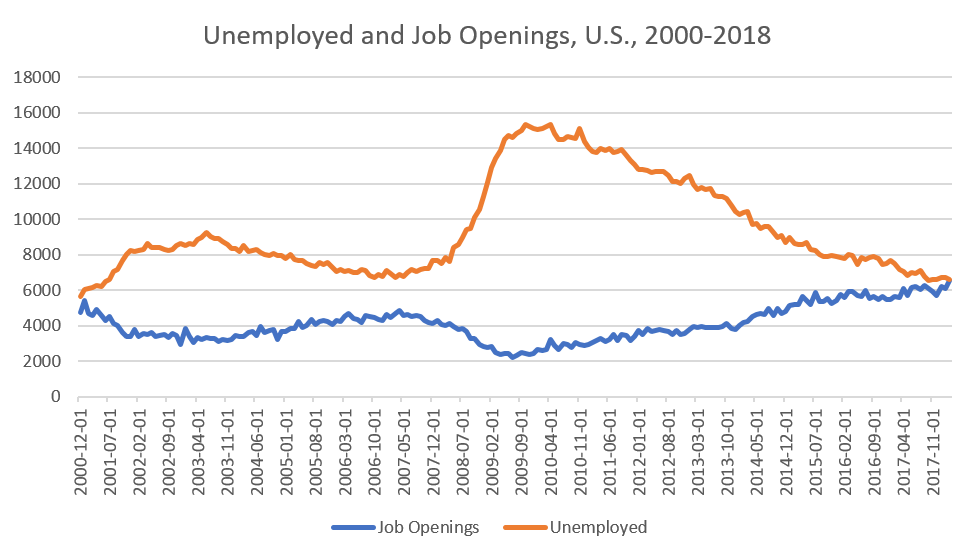

By all conventional measures, this is as strong a labor market as we’ve seen in decades, even in generations. The 3.9% official unemployment rate is the lowest since the tech boom of 2000. The gap between job openings and the number of unemployed was nearly 13 million (12,952,000 to be precise) in October 2009. It is virtually zero today (35,000—see the Chart below).

Source: U.S Bureau of Labor Statistics

Source: U.S Bureau of Labor StatisticsWait, there’s more. Continuing claims for unemployment insurance are the lowest since 1973, and initial claims for unemployment insurance are at the lowest since 1969. And today’s US labor force is twice the size it was back then. So, the data all point to a very tight labor market, and when demand for workers is rising relative to the supply of workers, the market responds by raising the price of labor (wages) and by attracting more supply (workers) into the workforce. That’s the way it should work, that’s the way it has always worked, but that is not how it is working now. Wages are rising only modestly, and the pool of available labor is shrinking. Hence, we see economists scratching their heads.

Wages are up 2.6% over the past twelve months, which is ahead of inflation (2.4%), but only modestly. Given how tight the labor market is, we would expect to see wages rising much faster. The answer to this riddle is hard to solve definitively for two reasons. First, this is a complex market, meaning there are many, many factors that weigh on demand and supply of labor, and linking specific variables to specific outcomes is nearly impossible, certainly not linearly. Secondly, proving causation is even harder, even if it were possible to draw a linkage between data.

That said, there are plausibly three broad trends that logically have combined to suppress wages: the decline in collective bargaining, automation, and global labor arbitrage. All three phenomena have been in place for decades. Union membership in 1983 (the first year the BLS collected data) was 20.1% of the workforce. It has fallen nearly in half, to 10.7%, today. For the private sector, just 6.5% of employees are unionized (it’s 34% in the public sector). We talked about the rise of robots back in 2015 (https://angeles-srv.s3.amazonaws.com/content./1441741791./2015-2.pdf), and that trend has only accelerated in the interim. The global labor arbitrage speaks directly to the forces of supply and demand. The collapse of the Soviet bloc in 1989 and the addition of China to the World Trade Organization in 2001, especially, brought billions of new workers into the global economy, nearly doubling the worldwide supply of labor. Our continued insistence on viewing markets domestically that have, in fact, become global, means we miss the important impact globalization, by expanding the labor pool, has had on workers.

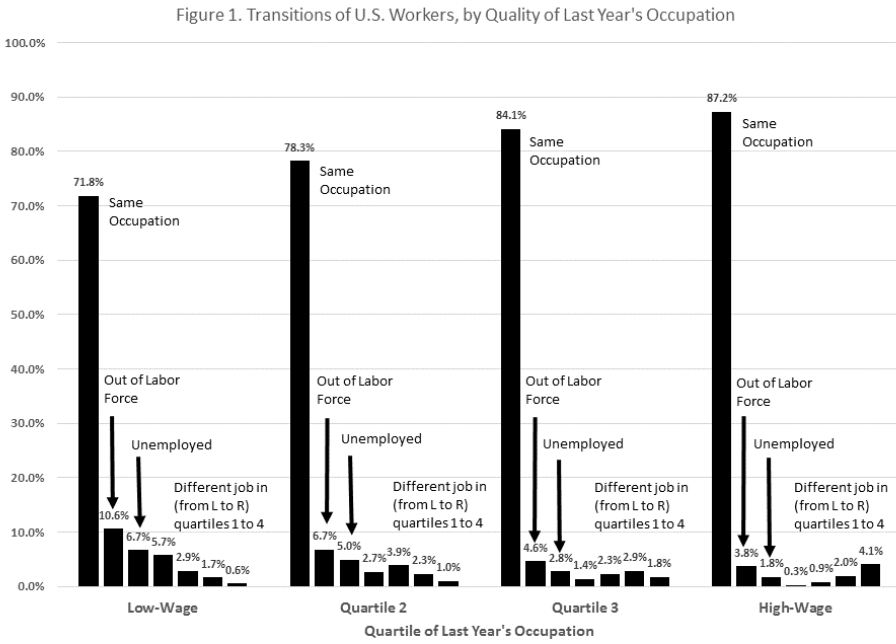

Wages have advanced modestly in this economic recovery, for whatever various reasons, but of perhaps greater concern is why it has become so difficult for low-wage employees to move into higher-wage jobs. We wrote last year about the decline in generational income mobility in America (https://angeles-srv.s3.amazonaws.com/content./1509463701./angeles-commentary-3q.pdf), and a new study by the Federal Reserve Bank of New York (Can Low-Wage Workers Find Better Jobs?, FRBNY Staff Report No. 846, April 2018) highlights how few low-wage workers move to higher wage jobs. Among the lowest quartile earners, in the past year 70% stayed in the same job, 11% exited the workforce, 7% became unemployed, and 6% switched to another lowest wage-quartile job. Only a little over 5% found a better job (see graph below).

These researchers point to a lack of formal education as the principal barrier to finding a better paying job, and also note that older workers are much less likely to move up the wage ladder. Interestingly, sales positions offer better prospects for advancement, and developing interpersonal (“sales”) skills could be an important path for many low-wage workers.

The other “mystery” puzzling economists is why the tight labor market has not drawn more workers into the labor force. At the peak of the last boom in 2000-2001, more than 67% of the population was in the labor force. Today, that has fallen to just 62.8%, barely up from the low of 62.3% seen in September 2015.

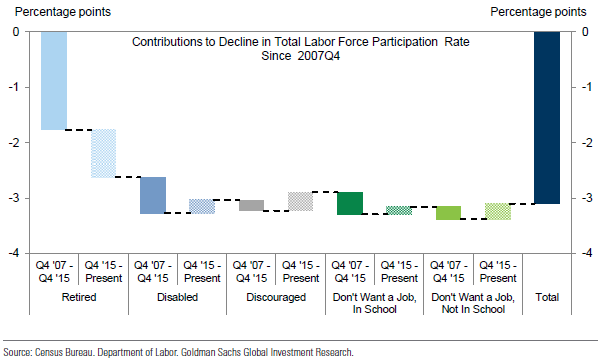

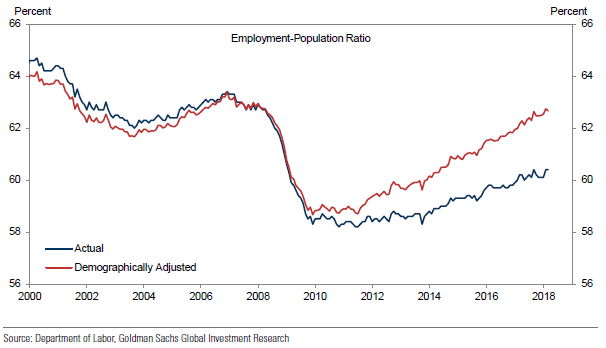

Now, a lot of the explanation for the low participation rate is demographic. Over the past decade, more than half of the decline is attributed to retirements (first graph below). On an age-adjusted basis, the labor participation rate has almost fully recovered to 2007 levels (second graph).

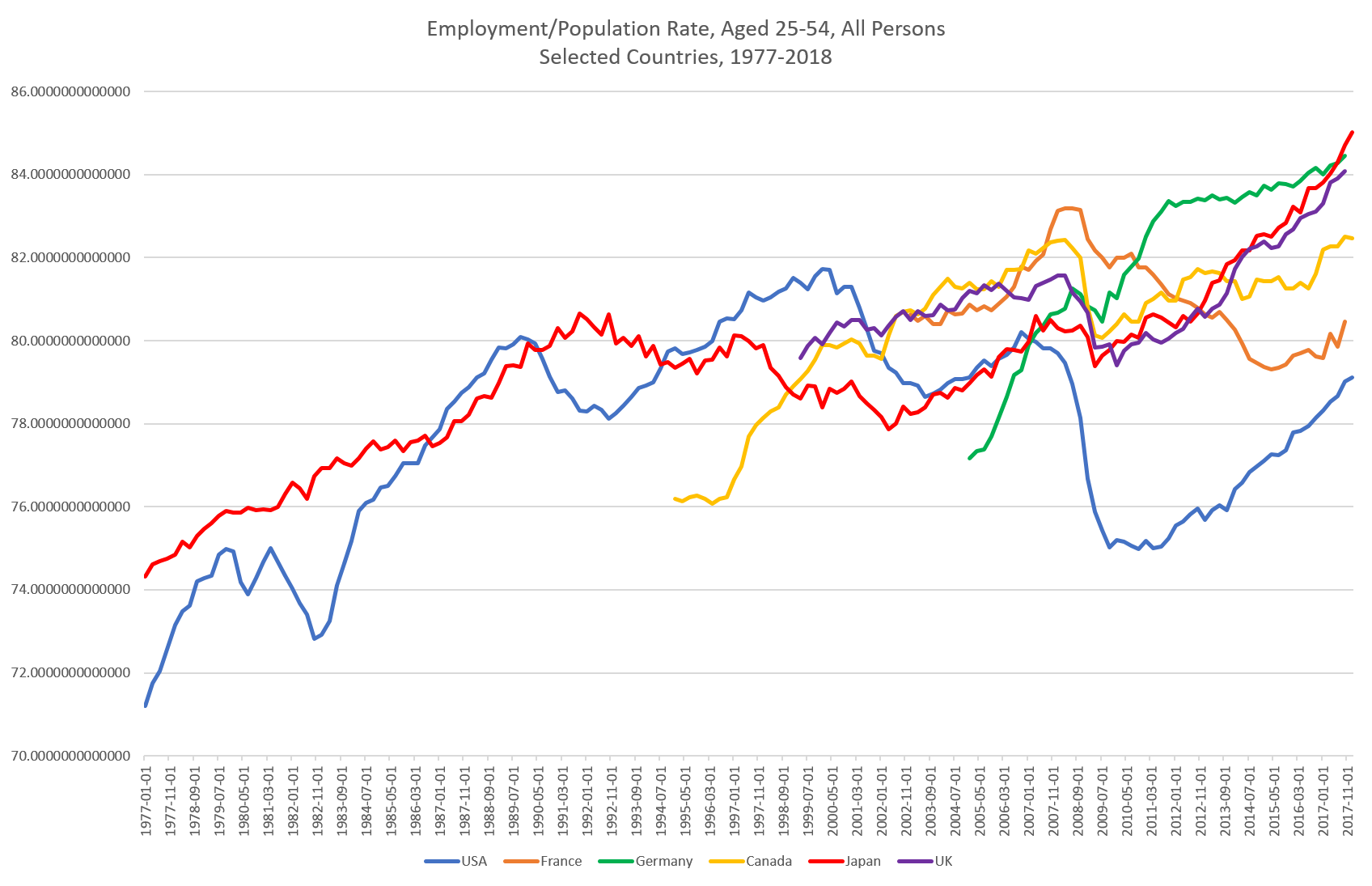

To examine the dynamics of the labor force more closely, we can put aside demographics by looking at data for prime-aged (25-54 years) workers. Despite a much weaker job market in Europe, where the unemployment rate stands at 8.5%, the participation rate for prime-aged workers exceeds that in the US (even in France, mon dieu!—see graph below for selected major countries).

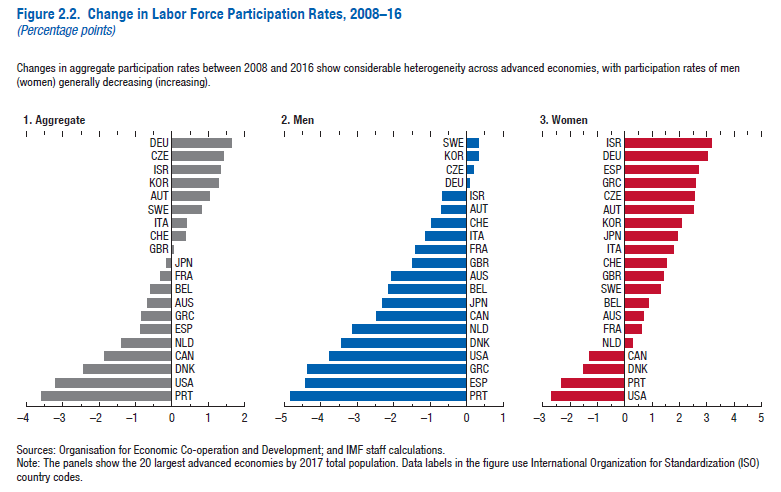

Over the past decade in advanced economies, we see a sharp divide in the change in participation rates among men and women. In most countries, the participation rate for men declined, whereas it increased for women. But in the US, which saw the second largest overall decline in the participation rate in the OECD (behind Portugal), declines occurred for both men and women (graph below). So there’s something going on in the US that’s not explained by age and gender.

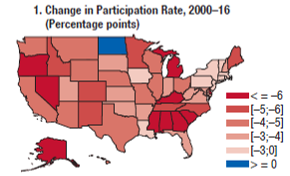

We have written extensively over the past year-plus(https://angelesadvisors.com/insights/#highlights) about the unique factors in the US that have worked collectively to reduce the labor supply among prime-aged workers, including high levels of incarceration, disability and addiction. To this, we can add a rural-urban divide. The fall in the labor force participation rate from 2000-2016 was widespread: every state saw declines (see graph below) but North Dakota (where there was a boom in shale oil production in the Bakken) and DC (tracing the inexorable growth of the federal government).

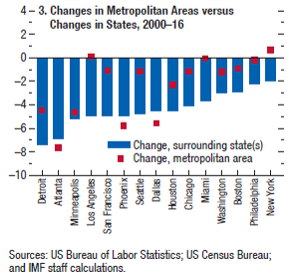

But participation rates in major cities were mostly much stronger compared to their surrounding areas. The graph below shows only three of the fifteen largest cities saw bigger declines than their surrounding areas (Atlanta, Phoenix and Dallas), where two (Los Angeles and New York) posted increases even as their regions saw declines.

The drop in the percentage of people working has enormous and widespread implications, both short-term and long-term. In the near-term, it may be driven by deeper structural problems, such as the afflictions of addiction and despair that tear apart communities. In the long-term, our societies are organized around people working: we rely on income to consume goods and services, we donate excess income to charities or save it for future uses, we tax income to fund government, entire communities are built around a dominant employer or industry.

The decline in labor force participation has many causal roots, and we need to consider the possible remedies for each one. To address the aging of our populations, we could expand tax credits for children, or welcome more (and younger) immigrants. To increase the percentage of women in the workforce, as has occurred in most other countries, perhaps better access to childcare, or more flexible work schedules, could be encouraged. Incarceration and drug dependency are crises in need of remediation for their own sake, even more than for the impact on the labor pool. Tax policy, based on workers’ incomes to fund Social Security and Medicare directly (and most of the rest of government in aggregate), needs to be re-thought in a world of fewer workers and more dependents. Would a tax on wealth, instead of income, be a better framework?

I do not mean for any of the above to be policy prescriptions or recommendations, only to say that the decline in the labor force participation rate is one of those economic data that gets little attention but has enormous consequences.

The title of this post references a 1959 hit song by Frank Pingatore, who was Bill Haley’s barber and songwriter (in that order). Frank re-wrote a song called Around the Clock Blues for Bill Haley and the Comets in 1955, re-titling it Rock Around the Clock. Frank wrote Everybody Out’ta the Pool for Bill Haley and the Comets, but Bill wanted no part of it, so the Comets recorded it as The Lifeguards, their one and only (modest) hit. But with Bill Haley out of the pool, the Comets, the Lifeguards, and even Bill Haley languished on in relative obscurity until Bill’s death in 1981. A fate our economy faces if we don’t find ways of getting more people back into the pool.

Print this Article

-

![Job Growth is Falling. The Sky is Not.]() 2 Jun, 2017

2 Jun, 2017Job Growth is Falling. The Sky is Not.

Today's jobs report was disappointing: only 138,000 net new jobs created in May (the consensus had it pegged at ...

-

![Yogi]() 24 Sep, 2015

24 Sep, 2015Yogi

Baseball, more than any other sport, by far, has drawn its share of colorful characters. I don't know why that is, but ...

-

![Inside the Triangle]() 23 May, 2016

23 May, 2016Inside the Triangle

Complexity makes investing so challenging. Unlike the pure sciences, there are no hard truths in investing, no ...

-