-

-

![Michael Rosen]()

-

CIO Insights are written by Angeles' CIO Michael Rosen

Michael has more than 35 years experience as an institutional portfolio manager, investment strategist, trader and academic.

RSS: CIO Blog | All Media

Rebalancings

Published: 03-16-2015Apologies for slipping on the blogs, but I’ve been traveling around the continent, from Alaska to DC.

One of the more common questions/comments we’ve heard from clients this quarter relates to the alleged benefit of global investing. Of course, this follows a year in which US equities gained 13% and non-US stocks fell about 5% (in USD terms), the widest performance gap since the 1990s. As usual, there were many valid reasons for this gap: the stronger economic growth and higher interest rates in the US favored dollar-based investors. And economic prospects, if anything, reinforced these trends: the gaps only widened in the second half of the year, promising a continuation of the trends favoring USD investors.

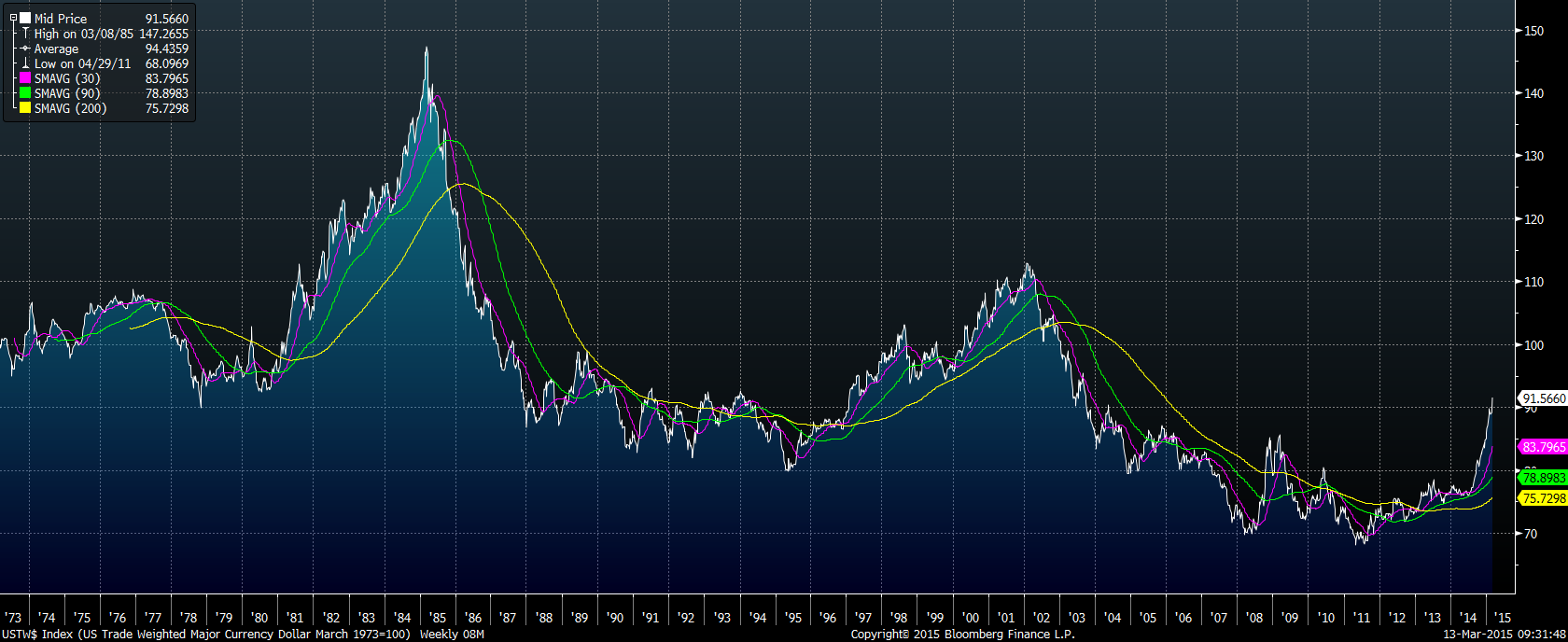

The dollar broke out of a long downturn last year (see graph below), accelerating at the fastest pace in the past six months since floating exchange rates were established in the early 1970s.

But markets (eventually) price in relative conditions, and the persistent weakness of the European economy and rising strength of the US economy were well understood by markets. As investors, it’s not enough to foresee the future (that’s hard enough). Success requires understanding what outcomes are already in prices. When the skew is sufficiently extreme, the successful strategy may be against the market, even if conditions do not yet support a change.

A great example was in early 2009, when credit spreads were wider than even during the Great Depression. At the time, the economy was a mess and the financial system a complete disaster, and the path out of the calamity was not clear. But the markets were pricing in an outcome that would be worse than the Great Depression. So even without confirmation of improvement, the successful strategy was to invest in those high spreads.

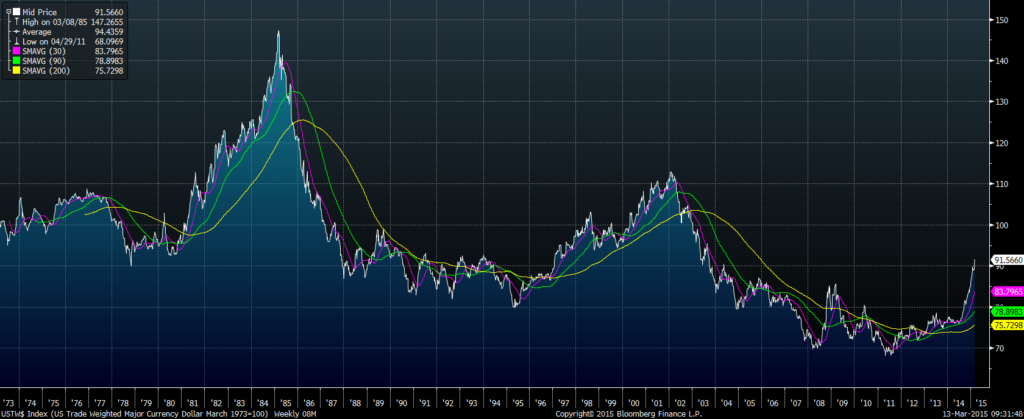

This year, we’ve seen something similar, on a much smaller scale, of course. The “Death of Europe” theme and the “Revival of the US” theme have been questioned, with current conditions, at the margin, improving in Europe and slowing in the US (see graph below).

Market prices are set at the margin, so one doesn’t have to believe that the European economy will outperform the US economy (I’m pretty sure it won’t over almost any time period). But when conditions go from worse to bad, that’s an improvement, or from great to good, that’s a regression, and that’s what we’ve seen this year in Europe and in the US.

Through today, European equities are up 11.5% YTD, 1000 basis points ahead of the US market. So the marginal improvement in the European economy relative to what was expected, is reflected in the markets, all as we would expect.

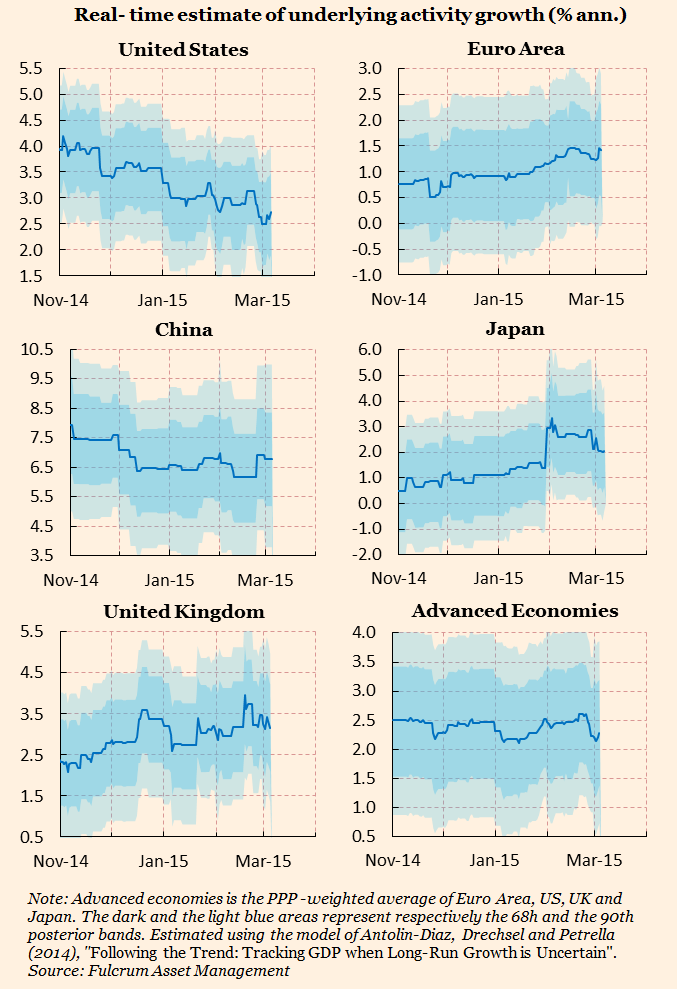

For investors, though, it’s never quite so simple. The rise in European equities has been accompanied by a decline in the currency (see graph below). That 11.5% equity return in euros translates to a 2% return in dollars, not much different than the 1.5% YTD return in the US market.

Trying to tie all this together, our portfolio tilts are generally pretty modest. Yes, economic conditions are improving a bit in Europe and slowing a bit in the US, favoring European assets, but the structural obstacles in Europe, political and economic, near- and longer term, are formidable, and I learned long ago as a currency trader not to step in front of a strong trend, in this case, to bet against the dollar. So I don’t see the reward in sticking one’s neck out in today’s markets, but yes, I still believe strongly in the value of diversifying globally because, one never knows.

Print this Article-

![Shades of 2007?]() 17 Oct, 2014

17 Oct, 2014Shades of 2007?

Nice graphic in today's FT showing the spike in vol and sell-off in risk (Greek bond yields jumped from 5.5% to 9% in ...

-

![Talkin' Turkey]() 14 Aug, 2018

14 Aug, 2018Talkin' Turkey

The expression comes from Colonial America, but its exact origins are unclear, and its meaning seems to have changed ...

-

![Only the Lonely]() 4 Feb, 2019

4 Feb, 2019Only the Lonely

My first impression when flying into Mexico City a few weeks ago was its vastness. From the air, the city seems to ...

-