-

-

![Michael Rosen]()

-

CIO Insights are written by Angeles' CIO Michael Rosen

Michael has more than 35 years experience as an institutional portfolio manager, investment strategist, trader and academic.

RSS: CIO Blog | All Media

Valuation

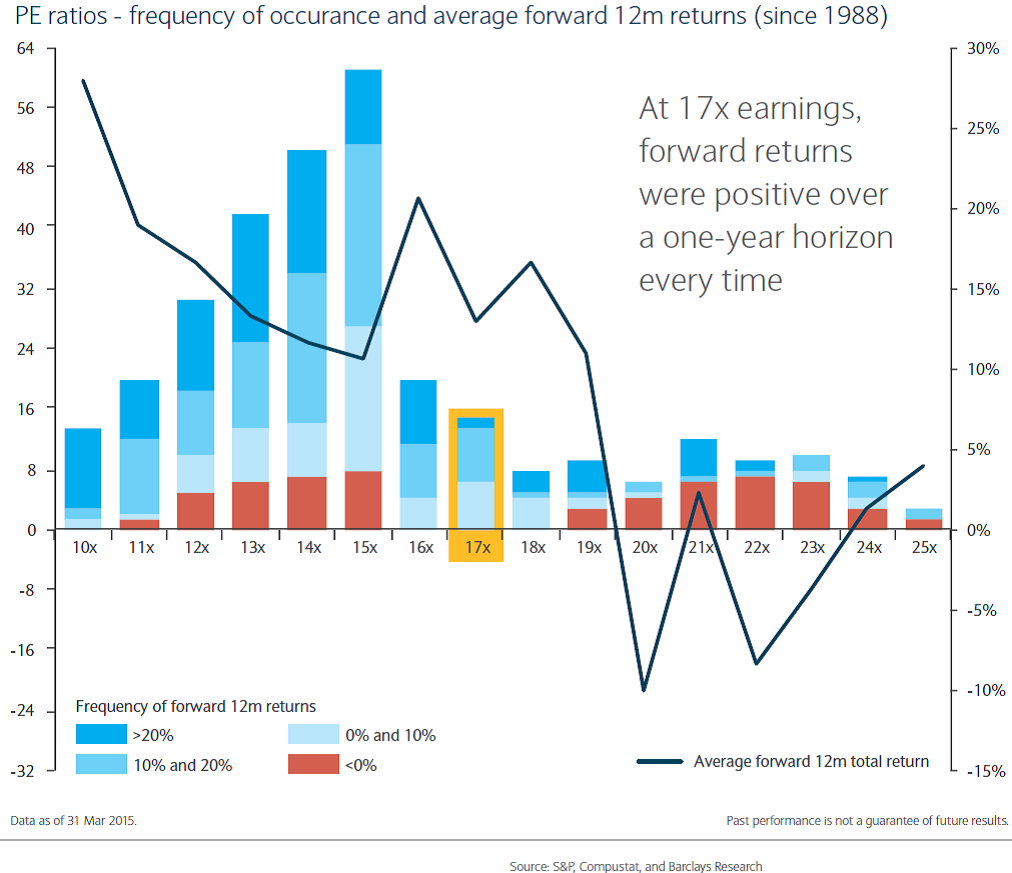

Published: 04-21-2015Most observers would agree that equities are rich (expensive, overpriced, etc.). Corporate profits are at record highs, and the forward price-to-(optimistic) earnings multiple on the S&P 500, at 17x, is the highest since 2004.

A favorite counterargument is a relative one: stocks may be expensive, but bonds are way more overvalued. With a 2% yield, the 10-year Treasury has a P/E multiple of 50x (taking the inverse of its yield). Of course, German bunds have an infinite P/E (with its negative yield). So stocks are the cheapest house in an expensive neighborhood.

That may be true, but this counterargument isn’t really a “counter,” i.e., stocks could still be expensive on their own even if other asset classes are more expensive.

The chart below (courtesy Barclays) shows the number of monthly observations of the S&P 500 at various forward P/E multiples (left y-axis). The subsequent average 12-month return is depicted by the black line (scaled to the right y-axis). And the range of subsequent 12-month returns at each P/E multiple is shown by the colors of each bar.

I like charts that convey a lot of information simultaneously (as this does), and this one leads me to three observations. The first two are pretty obvious/intuitive, the third, a bit more interesting:

- average future returns are higher when multiples are cheap than when multiples are expensive;

- negative forward returns can occur from both cheap and expensive multiples, although are more common when starting from an expensive base;

- forward returns have always been positive when multiples are in the middle range of valuation (as we are now).

I have not seen a rigorous study to explain this third point, but I’d speculate that the middle ground of valuation reflects an equilibrium environment that balances the macroeconomic risks of growth and inflation.

Of course, no law governs this observation, and the future path of equity prices is unknown. But in weighing the evidence, I see no compelling reason to deviate from our long-term strategy.

Print this Article

-

![Beach Reading]() 8 May, 2024

8 May, 2024Beach Reading

I'm happy to go to the beach year-round, but it's now really becoming beach weather, so I have five new book suggestions ...

-

![Book Wrap]() 31 Dec, 2018

31 Dec, 2018Book Wrap

Time for my semi-annual book perspective. I read a lot of books, but truthfully, most of them I move through pretty ...

-

![Energy Panic]() 16 Dec, 2014

16 Dec, 2014Energy Panic

Take a look at the price of a barrel of good ol West Texas Intermediate (see graph below). Two things jump out at me: ...

-