-

-

![Michael Rosen]()

-

CIO Insights are written by Angeles' CIO Michael Rosen

Michael has more than 35 years experience as an institutional portfolio manager, investment strategist, trader and academic.

RSS: CIO Blog | All Media

More on Rates...

Published: 06-26-2015A few days ago (Beginning’s End) I suggested 2015 might turn out to be the worst year for bond investors in the past three decades. Here are some additional pictures (courtesy of Goldman Sachs) to quantify the risks.

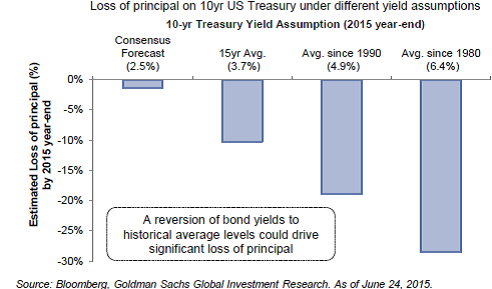

First we show the principal loss by the end of this year under various scenarios, with yields rising per current expectations or rising to historical means. The consensus expectation is for a loss greater than the current yield. Should yields revert to any of the historic means, losses would be greater.

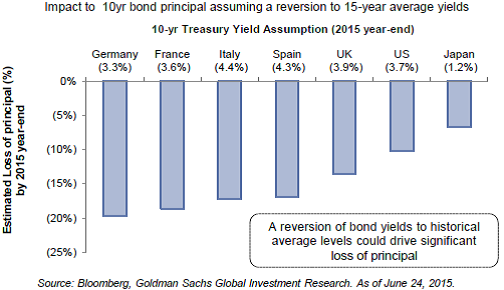

Before the tears start flowing, though, consider that US investors are likely to see losses much less than our European friends. Germans, for example, could be looking at another 20% loss of value (see Graph below). This is, of course, because US yields are substantially higher than other developed countries. At 2.47% (today), the 10-year Treasury yields more than comparable bonds in Spain or Italy (each with 10-year yields of 2.1%). French OATS yield just 1.2%, German bunds just 0.8% and JGBs 0.5%. The US offers the highest yields in the OECD.

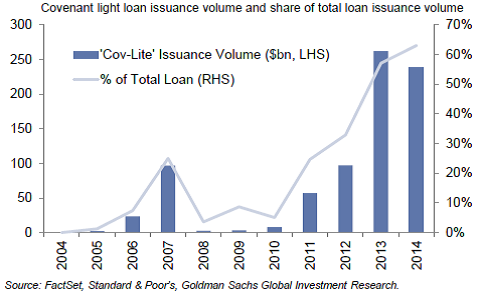

In addition to principal loss should interest rates rise, investors should also pay attention to the froth bubbling up in the high-yield (nee, “junk”) market. Loans with few, or any, covenants are at record levels, multiples ahead of the pace in 2007.

Our advice for bond investors? Caveat Emptor.

Print this Article-

![Truth and Consequences]() 3 Mar, 2019

3 Mar, 2019Truth and Consequences

Archaeological evidence suggests that, for thousands of years, the people who inhabited the Great Plains of North ...

-

![Only the Lonely]() 4 Feb, 2019

4 Feb, 2019Only the Lonely

My first impression when flying into Mexico City a few weeks ago was its vastness. From the air, the city seems to ...

-

![Weighty]() 8 Jan, 2015

8 Jan, 2015Weighty

Among new year resolutions, losing weight tops the list for the majority of Americans. Actually, I made up that ...

-