-

-

![Michael Rosen]()

-

CIO Insights are written by Angeles' CIO Michael Rosen

Michael has more than 35 years experience as an institutional portfolio manager, investment strategist, trader and academic.

RSS: CIO Blog | All Media

Janet Yellen Is Your Friend

Published: 09-28-2016I have not met Janet Yellen, but she seems like a perfectly friendly person. Yet, for some reason, investors seem to panic whenever she hints that the Fed is discussing whether and when to lift interest rates from close-to-zero to a smidgen above zero. That instinctive panic is not rational.

Part of the problem is that it appears there are so few people with a grasp of how monetary policy works, and certainly none who work in Congress or the media. So here’s a quick primer.

The Fed does not set interest rates. The Fed adds or withdraws reserves to or from the banking system, which has the effect of making more or less credit available to banks. When the supply of anything increases, its price falls, and vice versa. Adding more reserves to the banking system causes its price (the interest rate) to fall. Withdrawing reserves has the opposite impact. The Fed thus targets the price of overnight credit (Fed funds) through these liquidity operations, but doesn’t set it directly.

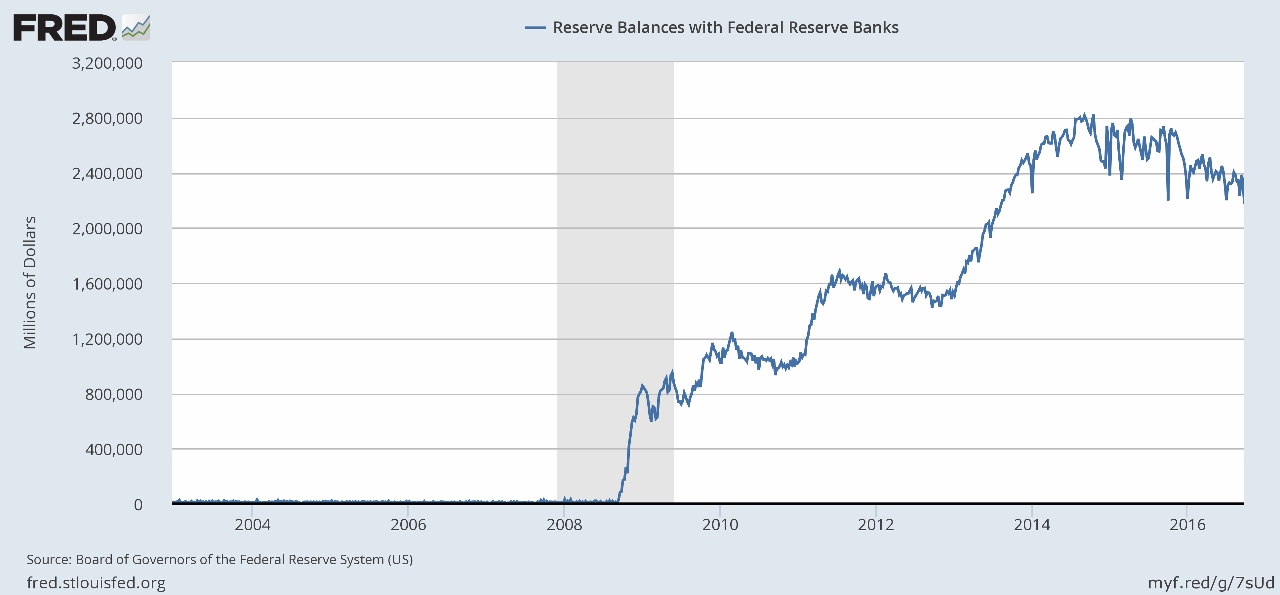

Beginning in 2009, and twice again later (QE1 and QE2), the Fed added reserves to the banking system (see graph below). Massively! Prior to the financial meltdown, reserves were minimal. They jumped to $800 billion in 2009, doubled to $1.6 trillion in 2011, and nearly doubled again to $2.8 trillion in 2014 (with the end of QE reserves have fallen to $2.2 trillion).

While the Fed can add reserves to banks’ balance sheets, they can’t make banks actually lend, or borrowers actually borrow. All those reserves the Fed injected pretty much stayed on banks’ balance sheets rather than feeding into the economy. In other words, the massive expansion of banking reserves had little (or no) impact in the real economy because those reserves were never turned into money, that is, circulating in the real economy. It was (is) an accounting gimmick.

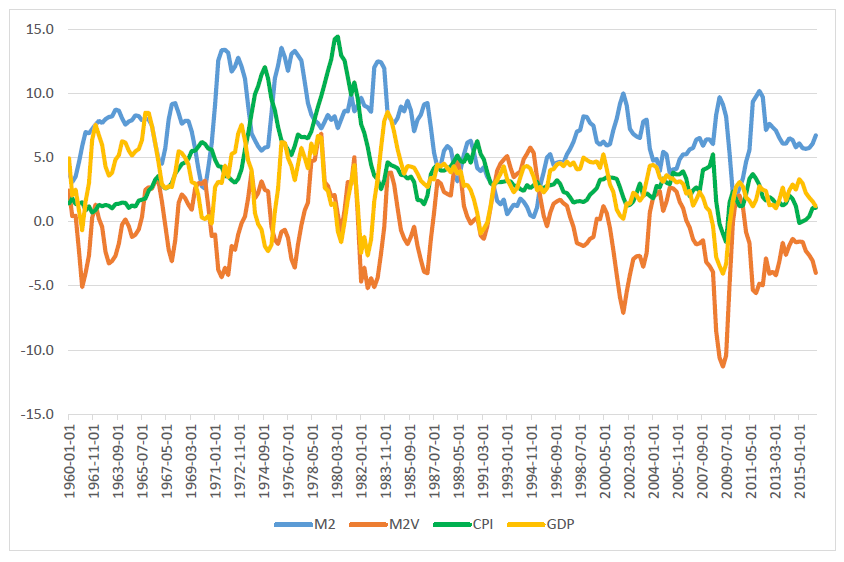

How do we know this? Well, I plotted a few variables to see what, if any, impact this enormous increase in banking reserves had in the real economy (see graph below—for comparison, each data series is expressed as percent change from a year ago). The blue line on top is M2, one measure of money supply. You can see that it has bounced around, and is currently growing near 6% p.a., right around its average of the past 20 years. Real GDP is the yellow line, and it has trended a little downward over the past 30 years, as has CPI, the green line. In other words, money supply growth has been pretty steady over the past few decades, while GDP and inflation have slowed. So the relationship, or correlation, between money supply growth and real economic growth or inflation is very weak. Why?

Well, there is no relationship between the change in money supply and real economic growth. There never has been. And there is no relationship between real economic growth and inflation. Again, there never has been (although this is one of the most enduring fallacies perpetuated by the ignorant). But there is a relationship between money and inflation, which is actually tautological, since inflation is, always and everywhere, in Milton Friedman’s famous phrase, a monetary phenomenon.

Why then has inflation fallen while money supply (M2) has been growing steadily? The answer is found in the orange line at the bottom of the graph: the velocity of money (M2) has been falling. The modest rise in money supply has been more than offset by a declining velocity of money. Thus, inflation has been falling.

Let’s go back to the first graph: reserves in the banking system have exploded. But with little (or no) effect on either economic growth or inflation. Would adding more reserves have any impact? No. Would withdrawing reserves from the banking system have any impact? No.

There are many reasons why economic growth is sluggish and inflation persistently below the Fed’s 2% target. Marginal changes in banking reserves is not one of them. When (if) the Fed decides to withdraw a few reserves to move the Fed funds rate a little higher, headlines will blare, pundits will shout and markets may gyrate, but the real economy will shrug. We have nothing to fear from the Fed. Janet Yellen is your friend.

Print this Article-

![Housing Has Legs]() 24 May, 2016

24 May, 2016Housing Has Legs

Surprisingly strong housing numbers out this morning: new single-family homes rose 16.6% in April to an annual pace of ...

-

![Consider]() 16 Oct, 2014

16 Oct, 2014Consider

Consider:Volatility spiked to its highest level in over 2 years.Global equities are in negative territory this year, led ...

-

![Fireside Reading]() 16 Dec, 2025

16 Dec, 2025Fireside Reading

As we approach the holiday season, I hope everyone has time to spend with family and friends, and a good book. Not ...

-