-

Investment Insight

3rd Quarter 2023 - Dyscrasia

Published 10-09-2023-

2023 3rd QUARTER QUARTERLY COMMENTARY

-

DYSCRASIA

![Dyscrasia]()

Records of infanticide, that most heinous of crimes, have, sadly, existed throughout human history. Disability and poverty have been common explanations for this horror, but so has misguided morality. Babies born in 18th and 19th century Europe out of wedlock were deemed "illegitimate," and were shunned by society, as were their mothers. In England, for example, the Bastardy Clause in the New Poor Law of 1834 made illegitimate babies the sole responsibility of the mother*, and both child and mother were banned from receiving aid.

As a consequence, cases of infanticide rose, and medical clinics to assist unwed mothers were started throughout Europe. At Vienna General Hospital two such clinics were established, one that trained doctors in obstetrics and other fields, and the second that trained midwives.

József Semmelweis was an ethnic German who had emigrated to Buda, capital of the Kingdom of Hungary, part of the Austro-Hungarian Empire. He was a grocer, and a very successful one**. He married another ethnic German, Teréz Müller, and they raised ten children in a prosperous household. The fifth child, Ignaz, studied law at the University of Vienna, but switched to medicine, graduating in 1844.

Ignaz found it difficult to secure a position. He failed to get an appointment in internal medicine, his first choice, but in 1846 he was named assistant (chief resident) in obstetrics at the First Obstetrical Clinic of Vienna General Hospital.

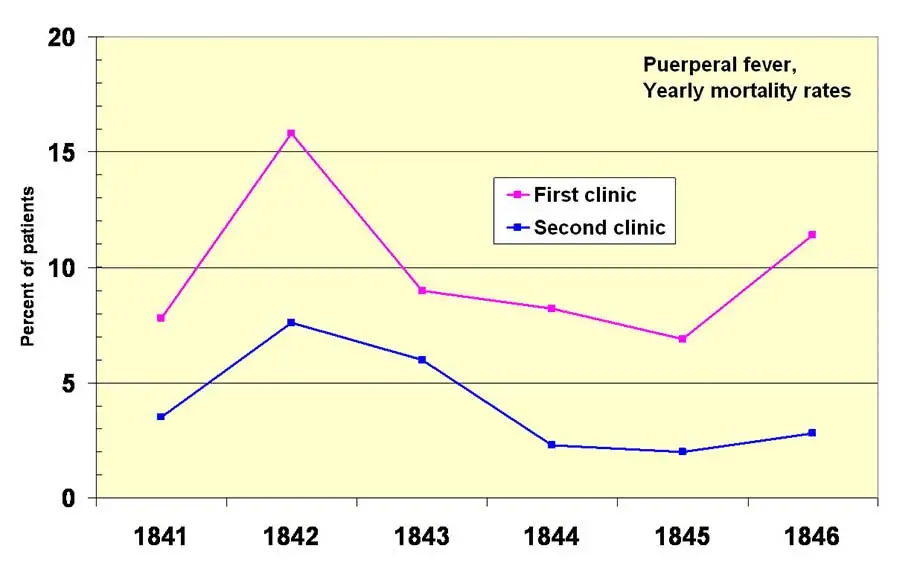

The clinics served primarily indigent women, including prostitutes. It was well known among these women that the First Clinic had a much higher degree of maternal mortality due to postpartum infection, or puerperal fever (Chart 1). Women begged to be admitted to the Second Clinic, even giving birth on the street in order to avoid the First Clinic where Ignaz worked.* Legislation written entirely by men.

** His store was called Zum weißen Elefanten (At the White Elephant).

- Chart 1

-

Annual Maternal Mortality Rates, First and Second Obstetrical Clinics, Vienna, 1841-1846

-

-

Source: Wikipedia

The Greek physician Galen* established that disease was caused by an imbalance of the four humors.** This imbalance was called dyscrasia, literally from the Greek, "bad" and "mixture." In the 1600 years following Galen, the medical establishment fully accepted his theory of dyscrasia. The doctors at Vienna General Hospital, to the extent they thought about it at all, ascribed the differing maternal mortality rates of the two clinics to a random distribution of dyscrasia. Blood-letting was the typical, if ineffectual, cure to restore the balance of humors in a patient.

Accepted wisdom is a dangerous proposition in investing, as it is in medicine. Common assumptions and explanations often appear legitimate for a time, or may have been erroneous all along. The practice of investment management is based on accepted assumptions and principles, many of which are valid, but some of which do not necessarily hold true, and lead, or ought to lead, to a re-examination of how we construct investment strategies. But questioning the assumptions of common wisdom is often fraught with personal peril, as Ignaz would discover.

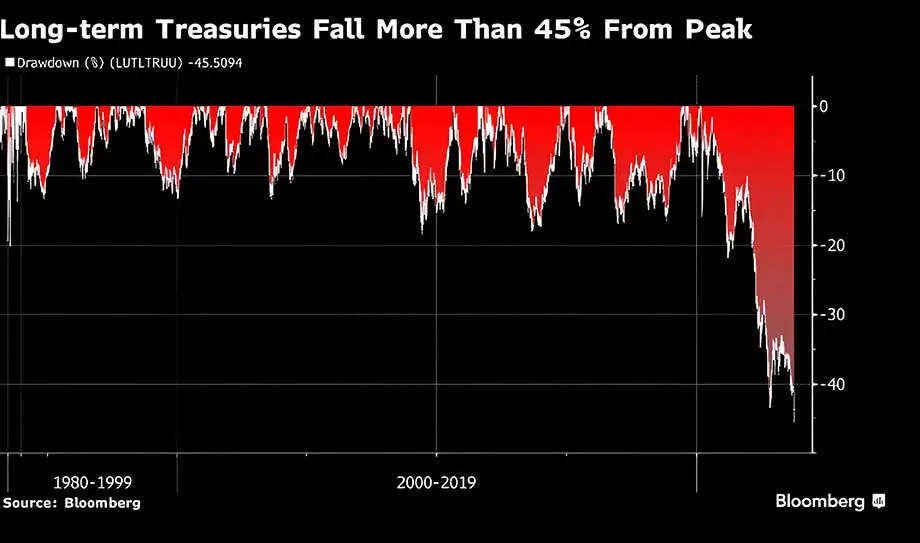

Government bonds have long played an important role in investors' portfolios, providing reliable income, price stability and a hedge when equities decline. But nearly three years ago***, we identified that conditions had changed: government bonds would no longer serve their central role in portfolio construction, providing neither income nor a hedge to equities, and they carried the prospect of significant capital losses.

We did not anticipate how correct this would be. Government bonds lost value in 2021, 2022, and are on track for a third consecutive decline for the first time in US history. The drawdown from the peak in June 2020 has been nearly 45%, more than twice as large as the declines seen in the 1970s (Chart 2). So much for safety of principal.* 129-216 C.E.

** Phlegm, blood, yellow bile, and black bile.

*** https://www.angelesinvestments.com/insights/angeles/a-new-framework-to-strategic-asset-allocation- Chart 2

-

Long-Term Treasuries Decline from Peak, 1979-2023

-

-

Source: Bloomberg

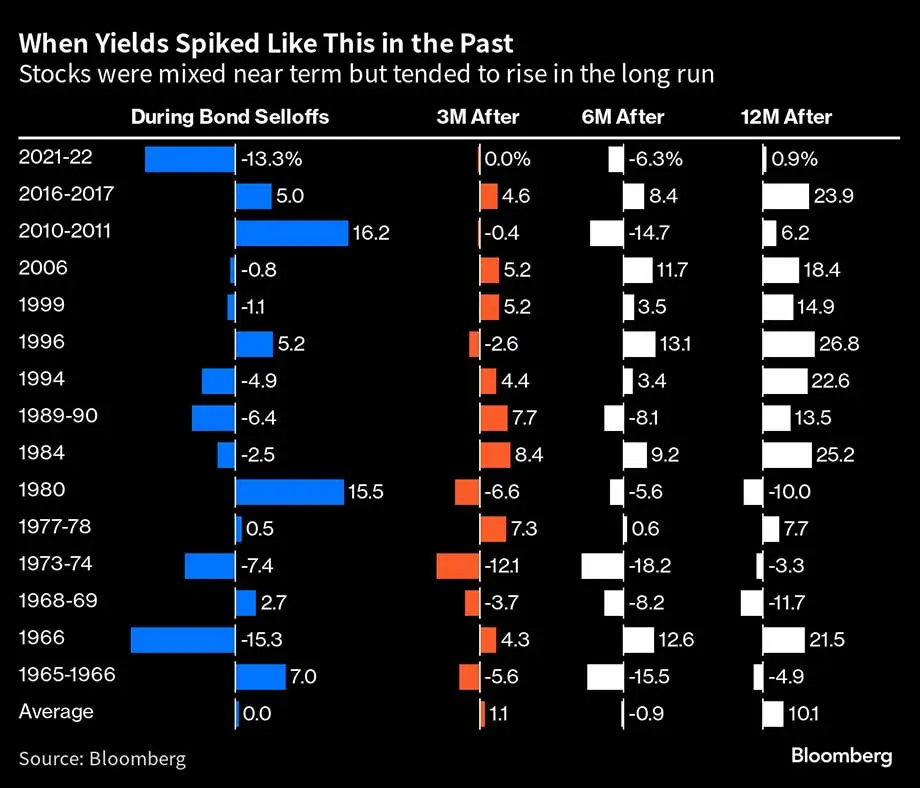

A silver lining for investors is that the dramatic drop in bonds does not necessarily lead to a sell-off in stocks. Since 1962, there have been 15 examples of five consecutive months of bond losses (2023 is the 16th such period). Stocks have had mixed results during those previous periods of bond declines, but twelve months out, equities were up an average of 10% (Chart 3).

- Chart 3

-

Stock Returns Following Bond Declines, 1962-2022

-

-

Source: Bloomberg

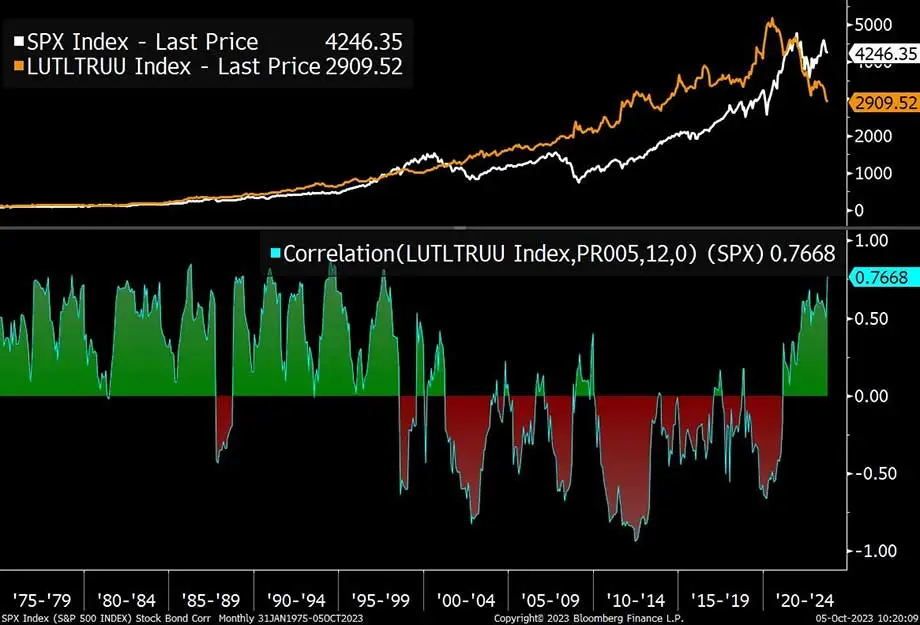

The loss in value of government bonds, as dramatic as it has been, is only one part of the problem for investors. For the past two decades, bonds have been negatively correlated with stocks, thus offering an excellent hedge to equity drawdowns. That has changed in the past few years as the correlation has turned positive (Chart 4).

- Chart 4

-

Correlation of Long-Term Treasuries to S&P 500 Index, 1975-2023

-

-

Source: Bloomberg

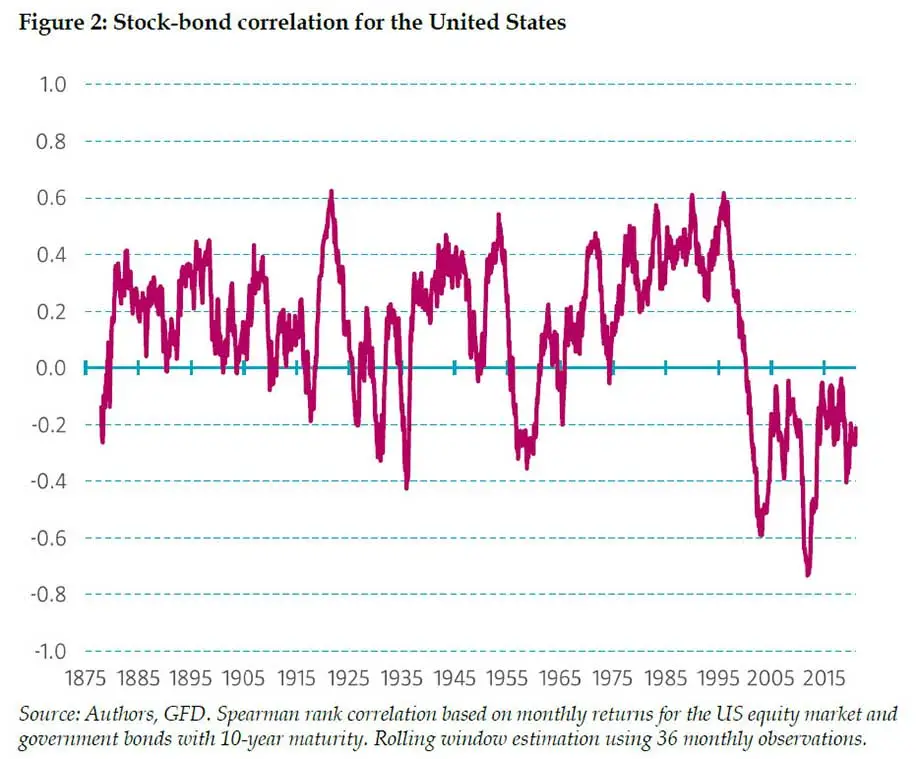

The past decade of negative correlation between stocks and bonds may prove anomalous. In the three decades prior to 2000, that correlation was positive, as Chart 4 shows. If we look further back, to 1875, we find a positive correlation between stocks and bonds more often than a negative one (Chart 5):

- Chart 5

-

Stock-Bond Correlation for the United States, 1875-2022

-

-

Source: Empirical Evidence on the Stock-Bond Correlation, Molenaar, et.al., July 2023, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4514947. Spearman rank correlation based on monthly returns for the US equity market and government bonds with 10-year maturity. Rolling window estimation using 36 monthly observations.

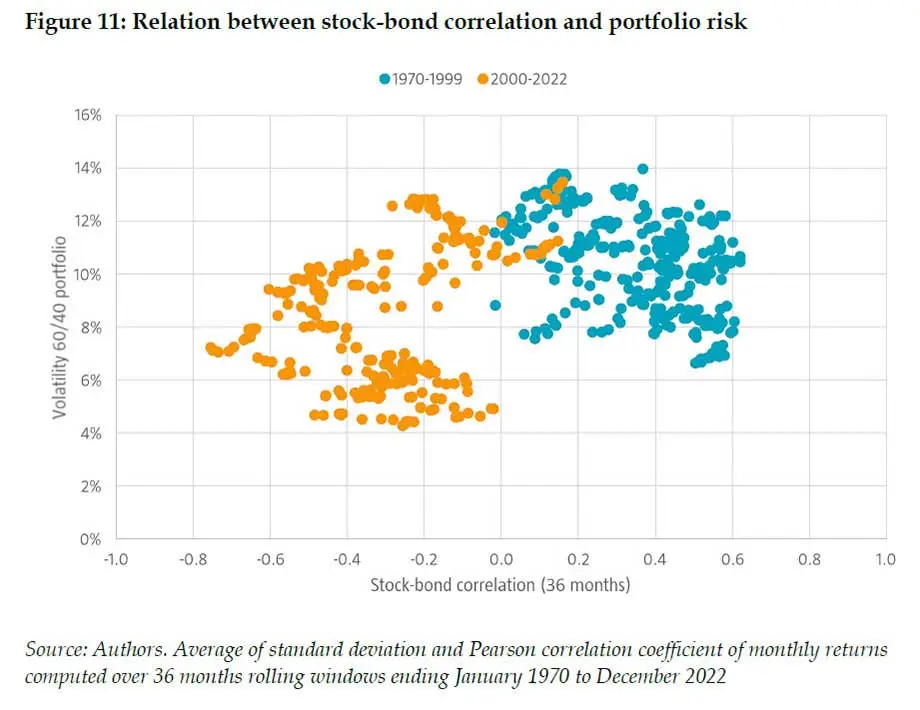

A positive correlation between stocks and bonds increases portfolio volatility (Chart 6), calling into question the validity, or certainly the desirability, of the traditional portfolio of equities and bonds.

- Chart 6

-

Relation Between Stock-Bond Correlation and Portfolio Volatility, 1970-2022

-

-

Source: Empirical Evidence on the Stock-Bond Correlation, Molenaar, et.al., July 2023, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4514947. Average of standard deviation and Pearson correlation coefficient of monthly returns computed over 36 months rolling windows ending January 1970 to December 2022.

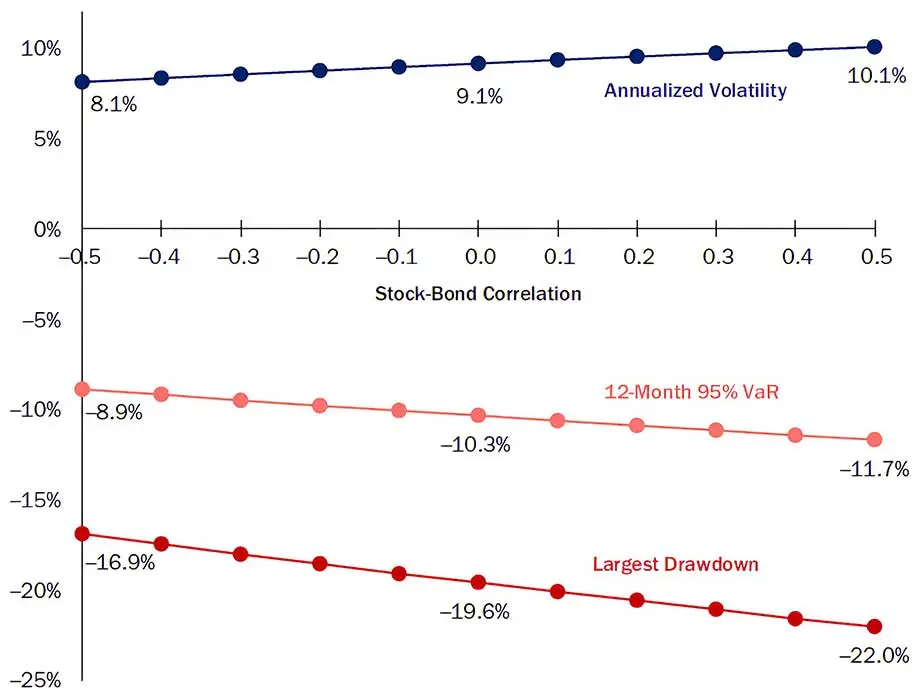

One model suggests that a rising stock-bond correlation could raise the volatility of a 60/40 (stock/bond) portfolio from 8% to 10% and increase the largest drawdown more than 5 percentage points (Chart 7).*

* A Changing Stock-Bond Correlation, Brixton, et.al., Journal of Portfolio Management, March 2023.

- Chart 7

-

Expected Risk of a 60/40 Portfolio

-

-

Source: A Changing Stock-Bond Correlation, Brixton, et.al., Journal of Portfolio Management, March 2023.

Inflation erodes the value of financial assets for investors, diminishes purchasing power for consumers and is the root cause of the changing correlation of stocks and bonds. This is proven by decomposing nominal bond yields into four components: the expected short-term rate, expected inflation, the real yield term premium and the inflation risk premium*. Higher expected yields and higher expected inflation are strongly related** to a rising stock-bond correlation (Table 1).

* The inflation risk premium is derived from the DKW model, in which nominal yields, real yields and inflation expectations are assumed to be linear functions of latent factors that follow a normal distribution. See this Federal Reserve paper for a description of the model: https://www.federalreserve.gov/econres/notes/feds-notes/tips-from-tips-update-and-discussions-20190521.html

** High t-stats.- Table 1

-

Correlation of Daily Values of Nominal Yield Factors with Stock-Bond Correlation, 1983-2023

-

![Dyscrasia]()

-

Source: Bloomberg

The old assumption that bonds would act as a hedge to equity declines has been proven false over the past three years. Rising inflation, and inflation expectations, have shifted the correlation between stocks and bonds from negative to positive, calling into question the assumptions underlying traditional portfolio construction.

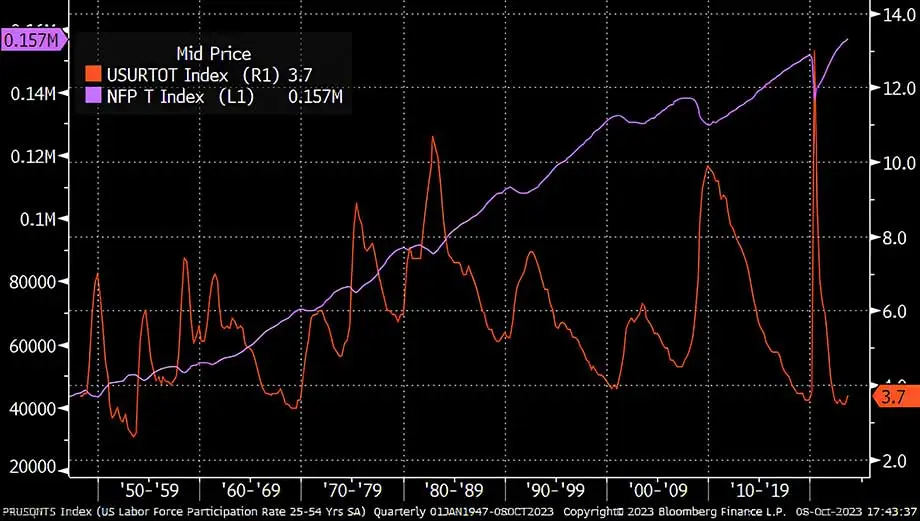

Recession has been forecast by economists for more than a year, and it has yet to appear. The US economy is exhibiting strength on numerous levels, starting with the labor market, where the unemployment rate (3.7%) is near record lows and the number of workers (157 million) is at an all-time high (Chart 8).- Chart 8

-

US Unemployment Rate and Non-Farm Employees, 1948-2023

-

-

Source: Bloomberg

The Phillips Curve is economists' standard model for describing the relationship (trade-off) between inflation and unemployment. Unfortunately (for economists) this is a terribly flawed model of how the real world works, as we've written.* In this model, a low unemployment rate is accompanied by high inflation, and vice versa. This ignores the 1970s when both unemployment and inflation were rising, and the subsequent decades when unemployment and inflation were falling together.

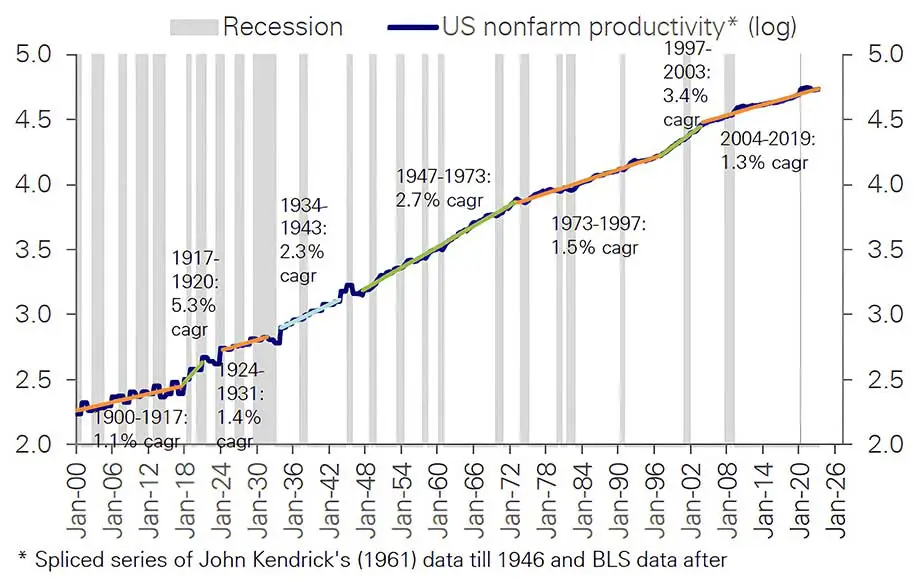

More importantly, tight labor markets have often been a precursor to rising productivity. And productivity is more than the key to rising living standards, productivity is axiomatic, definitional for improved living standards. Put succinctly, productivity is the reason we are all not subsistence farmers.

After a period of slow growth in productivity, we are likely entering a period of acceleration, spurred by significant advances automation, technology, genomics and AI (Chart 8).* https://www.angelesinvestments.com/institutional-insights/satisfaction

- Chart 9

-

US Non-Farm Productivity Growth, 1900-2022

-

-

Courtesy: Deutsche Bank

Ignaz could not accept that the high maternal mortality rate in the First Obstetrical Clinic was due to dyscrasia, a "bad mixture" of the four humors. The lower mortality rate at the Second Clinic belied that explanation. So Ignaz began a systematic review of the possible differences between the two clinics that would possibly explain the vastly different rates of puerperal fever.

Climate could be eliminated because the two clinics were in close proximity to each other. The Second Clinic was more overcrowded than the First Clinic, so overcrowding was not the cause. He noted that in the Second Clinic midwives had women give birth on their sides, so he instituted the same practice for women in the First Clinic. There was no change in puerperal fever rates. He then noticed that in the First Clinic when a woman died a priest would walk through the ward ringing a bell. Perhaps this frightened the other women who then caught puerperal fever, so Ignaz had the priest stop ringing a bell. It made no difference. The only difference that remained was that doctors were trained at the First Clinic and midwives at the Second Clinic. But Ignaz did not understand why that would be the explanation for, if anything, the highly trained doctors should deliver better care than the midwives.

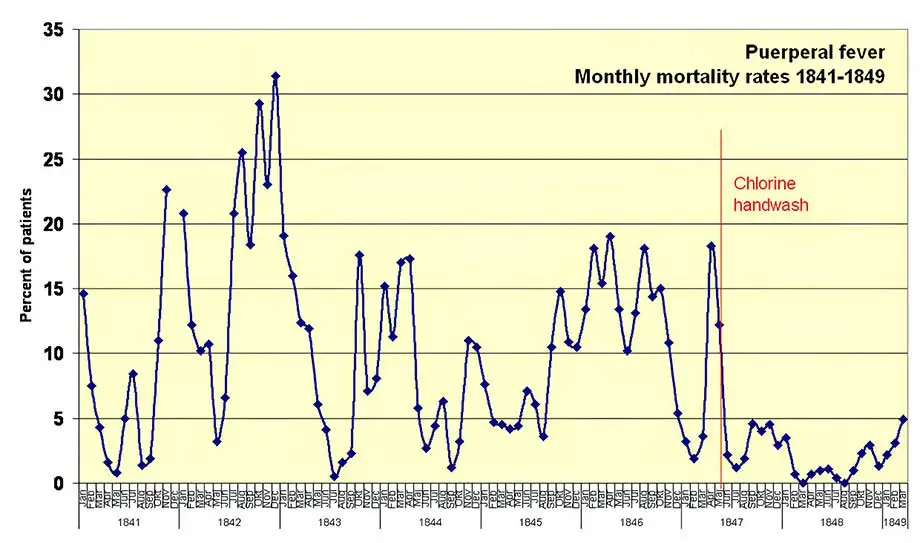

In 1847, Ignaz's good friend, Dr. Jakob Kolletschka, was conducting an autopsy with students when one of the students accidentally scraped the doctor with his scalpel. Kolletschka died shortly thereafter. An autopsy revealed that he died of a similar pathology as the women who died of puerperal fever. This pathology would much later be identified as the Streptococcus pyogenes bacteria. Doctors at the First Clinic routinely conducted autopsies, something midwives did not do, and would often go directly from a postmortem examination to the maternity ward. Ignaz proposed that there was a connection between cadaveric contamination and puerperal fever.

So Ignaz required doctors to wash their hands with a solution of calcium hypochlorite after each autopsy. This solution removed the putrid smell of infected cadaverous tissue that Ignaz guessed might be the cause of puerperal fever. In April 1847, before the hand-washing policy was instituted, the mortality rate in the First Clinic was 18% (not annualized, in the month!). The new procedure began in May and in June the mortality rate had fallen to 2%, then 1%, and even a few months with zero maternal mortality for the first time ever recorded (Chart 10).- Chart 10

-

Monthly Maternal Mortality Rates, First Obstetrical Clinic, 1841-1849

-

-

Source: Wikipedia

Ignaz expanded the protocol to include all instruments that came in contact with patients. Mortality rates dropped even further, although no one, including Ignaz, knew exactly why that was so. A few years earlier, the prominent American physician, Oliver Wendell Holmes, Sr.,* wrote a paper suggesting that puerperal fever was caused by physicians who had conducted autopsies and then examined patients, but he offered no explanation or suggestions on what should be done.**

Correlation is not causation, as investors (and doctors) have been told.*** It was widely accepted that dyscrasia, the imbalance of the four humors, caused disease. Ignaz's implication that doctors were the cause of spreading puerperal fever did not sit well with doctors. Ignaz was ostracized by his colleagues, and he didn't help his cause by denouncing the medical profession as ignorant. When his term was up at the First Obstetrical Clinic, he was not reappointed. Ignaz left Vienna to return to Hungary without a word of goodbye to his staff.* Father of Civil War hero and future Supreme Court Justice Oliver Wendell Holmes, Jr.

** The Contagiousness of Puerperal Fever, 1843.

*** Karl Pearson, the great British statistician who founded the first statistics department at University College London in 1911, was probably the first to warn of conflating correlation and causation.He took an unpaid position at a small hospital in 1851 where puerperal fever was rampant. He eliminated the disease there. Still, other physicians in Budapest did not adopt the hand-washing protocol, showing the same dislike of Ignaz and his ideas as the doctors in Vienna had.

Ignaz became increasingly vitriolic, accusing physicians of being murderers, or worse, ignorant murderers. He began to drink heavily, frequented prostitutes, perhaps contracting syphilis, and in 1865 his wife had him committed to an insane asylum where he was beaten by guards. He died two weeks later from those beatings of septic shock, the same infection that also causes puerperal fever. His death went unannounced and unnoticed.

At the time of his death, a scientist working in Paris was exploring the role of bacteria in fermenting wine. Two years later a Scottish surgeon, who had not heard of Ignaz, began promoting handwashing with carbolic acid before surgery. And in 1876, a German physician was able to link Bacillus anthracis to a specific infectious disease, anthrax. Thus did Louis Pasteur, Joseph Lister and Robert Koch establish the germ theory of disease, erasing 1600 years of Galen's dyscrasia theory, providing the scientific proof for the efficacy of Ignaz's handwashing protocol.

Ignaz Semmelweis challenged the established wisdom of the medical profession by questioning and examining their widely-held assumptions. He found those assumptions to be invalid and found a solution that worked, even if he didn't know exactly why. For this, he was despised and disgraced. And for this, thousands of mothers died needlessly.

Investors must navigate a world of uncertainty, where we make assumptions we believe to be valid, but may not be. This requires constant vigilance in testing those assumptions, and in having the courage to act when we see that accepted wisdom is wrong.

Also, wash your hands!

![Ignaz]()

![Wash your Hands!]()

-

![Michael Rosen]()

-

Michael A. Rosen

Principal & Chief Investment Officer

Michael Rosen, co-founder and Chief Investment Officer of Angeles Investments, has 37 years of experience as an institutional portfolio manager, investment strategist, and investment consultant.

Please see more insights from Michael Rosen and Angeles here:

www.angelesinvestments.com/insights/home -

October 2023

Connect with us

![Angeles on Linked In]()

Founded in 2001, Angeles is a multi-asset investment firm, building customized portfolios for institutional and private wealth investors.

This report is not an offer to sell or solicitation to buy any security. This is intended for the general information of the clients of Angeles Investment Advisors. It does not consider the investment objectives, financial situation or needs of individual investors. Before acting on any advice or recommendation in this material, a client must consider its suitability and seek professional advice, if necessary. The material contained herein is based on information we believe to be reliable, but we do not represent that it is accurate, and it should not be relied on as such. Opinions expressed are our current opinions as of the date written only, and may change without notification. We, along with any affiliates, officers, directors or employees, may, from time to time, have positions, long or short, in, and buy and sell, any securities or derivatives mentioned herein. No part of this material may be copied or duplicated in any form by any means and may not be redistributed without the consent of Angeles Investment Advisors, LLC.

If you would like, please click this link to receive a copy of our Form ADV Part 2A free of charge. -