-

Investment Insight

2nd Quarter 2024 - Verschlimmbesserung

Published 07-08-2024-

2024 2ND QUARTER QUARTERLY COMMENTARY

-

VERSCHLIMMBESSERUNG

General Motors dominated the American economy of the 20th century in ways that can hardly be imagined today. For more than half a century it was one of the two or three largest companies in America, with over 600,000 US employees, more than 850,000 worldwide. By the mid-1950s, GM controlled more than half of the auto market in the United States. For 77 years, 1931-2008, General Motors was the largest automobile manufacturer in the world.*

The company was founded in 1908 in Flint, Michigan by Billy Durant. Durant started as a buggy maker in 1886, took over the Buick Motor Company in 1904, and soon made Buick into the world’s largest automobile manufacturer. General Motors was his holding company, which soon acquired other auto manufacturers, including Olds, Cadillac and Pontiac. In 1919, Durant acquired Guardian Frigerator, renaming it Frigidaire, which so dominated the market that Frigidaire became the generic name for refrigerator**. GM branched into aviation with the 1929 acquisition of Allison Engine and the 1933 purchase of North American Aviation.

During World War Two, GM converted to a military supplier, hiring 750,000 workers, 30% of whom were women. GM built airplanes (the Grumman Avenger and Wildcat, and the iconic North American P-51 Mustang, the premier fighter of the war), tanks (including the famous M4 Sherman), artillery shells, rifles (the standard M1) and machine guns.

GM’s chairman, Charles E. Wilson***, served as Secretary of Defense in President Eisenhower’s first term. At his Senate confirmation hearing in 1953 he was asked if he could make a decision that would harm General Motors if it was in the interest of the United States. His famous reply was: “Yes, sir; I could. I cannot conceive of one because for years I thought what was good for our country was good for General Motors, and vice versa. The difference did not exist. Our company is too big. It goes with the welfare of the country. Our contribution to the Nation is quite considerable.”

General Motors achieved its dominance not just through the hard work of its thousands of employees, but also via innovations from some of the most talented engineers in the world. In the 1920s and 1930s, when General Motors was establishing its supremacy in the American economy, two particularly vexing problems threatened its success. The company turned to one of its most brilliant minds, whose eventual solutions ensured that General Motors would be the world’s leading manufacturer for decades to come. A man who would win every prestigious engineering award, a man whom Orville Wright called “a truly great citizen.” A man who ultimately may have been responsible for more deaths than any individual in history.

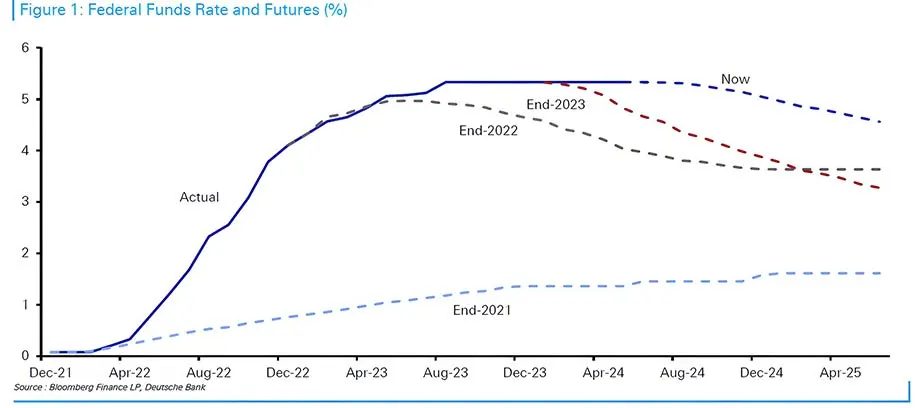

Market “experts” have long called for a reversal of three major “unsustainable” trends. First, that after the extraordinarily rapid rise in interest rates, more than 500 basis points in little over a year,**** rates are soon to fall (Chart 1).

* Supplanted by Toyota.

** Much like Kleenex tissues, or Hoover vacuums.

*** Known as “Engine Charlie” to distinguish him from Charles E. Wilson of General Electric, known, of course, as “Electric Charlie.”

**** From March 2022 to July 2023, the Fed funds rate rose from 0.25% to 5.5%.

- Chart 1

-

Fed Funds Rate and Futures, December 2021-June 2024

-

-

Courtesy: Deutsche Bank

The experts have been expecting the Fed to cut interest rates for the past two years in anticipation of falling inflation and an imminent recession. Neither have happened. Inflation has not been below 3% in over three years,* a record 161 million people are employed, and the “imminent” recession has not materialized. Why would the Fed cut interest rates in this environment? The experts have been, and continue to be, wrong about the direction of rates.

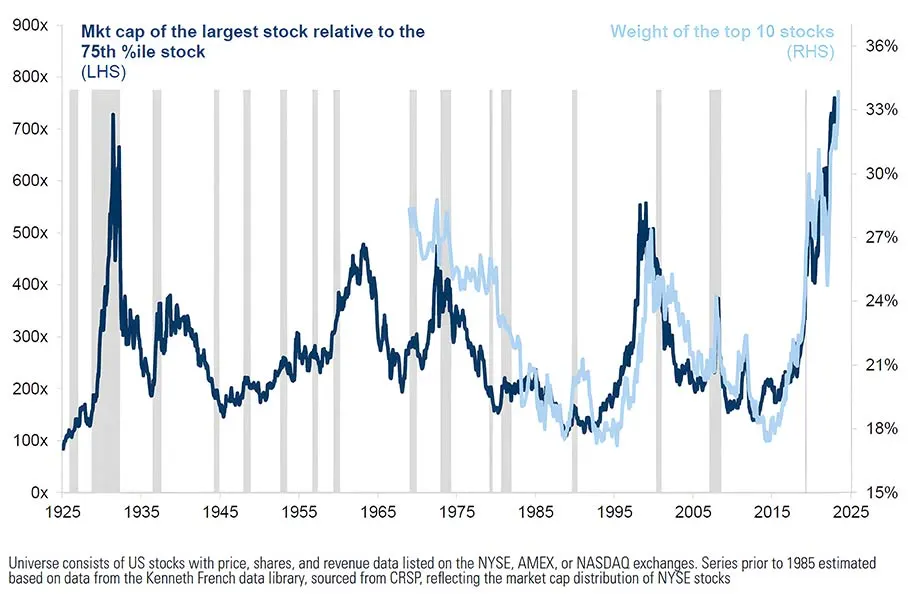

Concentrated market leadership, where a handful of stocks, mostly in the technology sector, account for the vast majority of the market’s gains, has been another warning of imminent market collapse by these same experts. Indeed, by some measures, market concentration is the highest it has been since 1929 (Chart 2), and that did not end well.

* March 2021 was the last reading of YoY CPI below 3%.

- Chart 2

-

US Equity Market Concentration, 1925-2024

-

-

Courtesy: Goldman Sachs

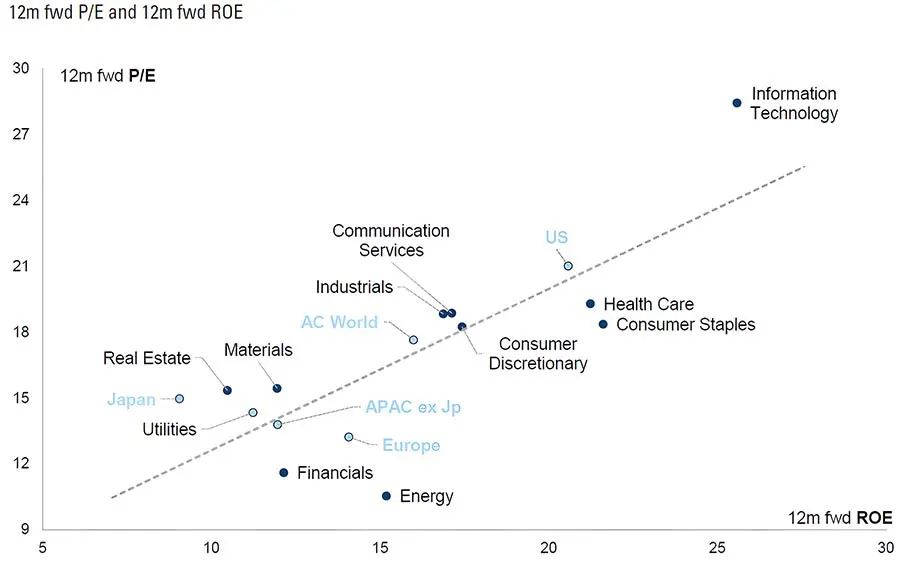

But the pundits have missed a few salient facts. Over the long-term, as the research of Hendrik Bessembinder has shown,* market gains are generated by a very small number of stocks. In other words, concentrated market leadership is the norm, not the exception. Today, the majority of earnings comes from a handful of companies, and the relationship between profitability and valuation does not look out of line (Chart 3).

* Bessembinder, Hendrik, Do Stocks Outperform Treasury Bills?, Journal of Financial Economics, January 2017: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2900447.

- Chart 3

-

12-month Forward P/E Multiple and 12-month Forward ROE

-

-

Courtesy: Goldman Sachs

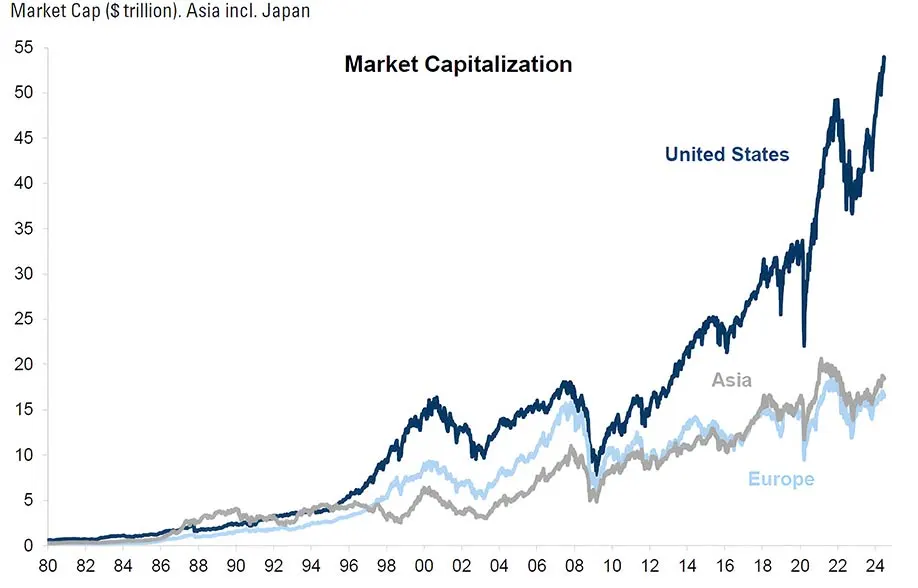

The third major trend experts have called for its reversal is the massive outperformance of US equities relative to the rest of the world. At the time of the Global Financial Crisis in 2008, the stock markets of the US, Europe and Asia were of roughly comparable size, all less than $10 trillion. Today, Europe and Asia are valued at around $15 trillion each, while the US market has soared to over $50 trillion (Chart 4).

- Chart 4

-

Market Capitalization, US, Europe, Asia, 1980-2024

-

-

Courtesy: Goldman Sachs

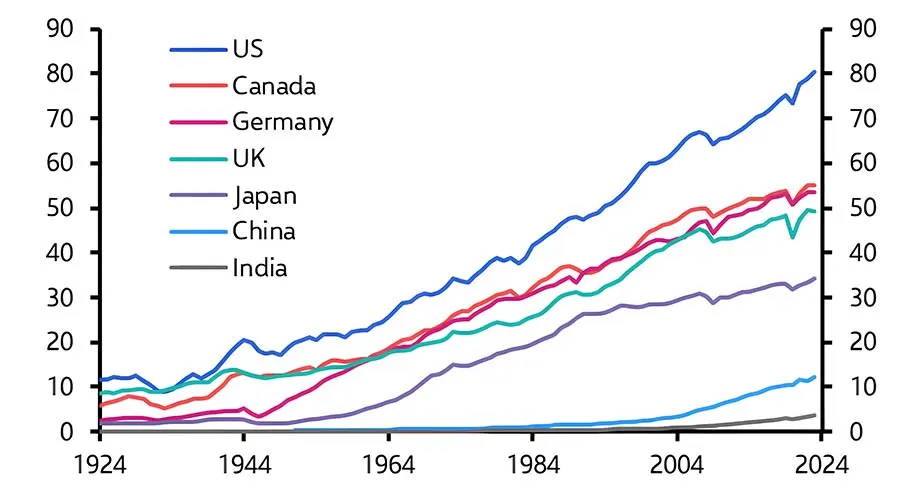

Rather than a cause for worry or a portend of imminent reversal, the outperformance of the US market reflects the higher profitability of US companies, as we’ve noted multiple times over the past few years.* It also reflects the widening gap in economic performance of the US over the rest of the world (Chart 5).

* https://www.angelesinvestments.com/insights/investment-insights/4th-quarter-2022-kapitalismus and https://www.angelesinvestments.com/insights/investment-insights/4th-quarter-2023-storms.

- Chart 5

-

Real GDP Per Capita, Select Countries, 1924-2024, $000, 2023 Market Prices and Exchange Rates

-

-

Courtesy: Capital Economics

An imminent recession, extreme market concentration and massive US outperformance are the basis for those who call for this structural bull market to end. History suggests otherwise. This bull market that began in 2009 (orange line, Chart 6) is closely tracking the bull market of the 1950s-1960s, and is well below the pace of the enormous structural bull market of the 1980s-1990s (Chart 6).

- Chart 6

-

Structural Bull Markets In the US, 1950-present

-

-

Source: Bloomberg Finance L.P.

One day, all these trends will reverse. Or not. No one really knows, and that is the point. Higher interest rates, market concentration and US outperformance all reflect fundamental economic forces at work.

Market prices will fluctuate, as J. P. Morgan famously (or apocryphally) said, but investors should focus on the fundamental drivers of market returns.

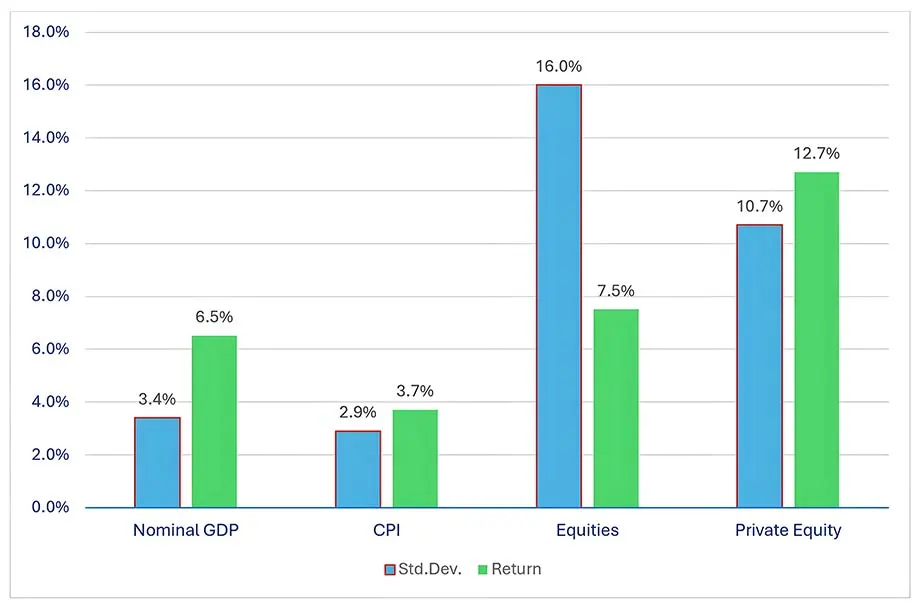

Fluctuation, or volatility, of economic data and market prices is caused by the shifting forces of supply and demand. The volatility, or standard deviation,* of the principal economic data of GDP and inflation is around 3% per annum. That is, most of the time,** annual GDP and inflation are +/- 3% around their means.

But the standard deviation of public equities is around 16% p.a., five times the volatility of the underlying economic data (Chart 7). Over the long-run, public equities will generate strong returns, in excess of economic growth,*** but investors are required to accept fluctuations in values that are orders of magnitude higher than justified by economic fundamentals.

* Standard deviation is the degree of dispersion around a mean. Its formula is:

![Formula]()

** “Most of the time” is specifically 2/3rd of the time.

*** Since 1946, nominal GDP has averaged 6.5% p.a. while the S&P 500 Index has returned 7.5% in price, 9.1% p.a. with dividends reinvested in the Index.- Chart 7

-

Standard Deviations and Returns of NGDP, CPI, Public and Private Equities

-

-

Source: Bureau of Economic Analysis, Bureau of Labour Statistics, MSCI, Cambridge, author's calculations.

Note: Nominal GDP 1954-2024, CPI 1948-2024, Equities (MSCI ACWI Index) 1999-2024, Private Equity (Cambridge Private Equity Index) 1999-2024. Source: Bureau of Economic Analysis, Bureau of Labor Statistics, MSCI, Cambridge, author’s calculations.

There is no simple explanation for why public equities are so volatile. The stock market is not the economy, that is, public companies represent a subset of overall economic activity, so we would expect a greater degree of volatility for a subset than for the whole. Behavioral factors, like sentiment, no doubt exacerbate market fluctuations. The very high volatility of equities, and their high returns, make equities suitable only for long-term investors.

Private equity has generated returns 3-5% p.a. higher than public equities with an observed standard deviation that is two-thirds that of public equities (Chart 7). Most institutional investors and consultants discount this “free lunch” of higher return and lower volatility by assigning, arbitrarily, a higher standard deviation to private equity when modeling asset allocation.

The assumption behind this discount is that private equity valuations are estimates at best, or may even be manipulated to dampen their “true” volatility. This has the effect of reducing the attractiveness of private equity in an asset allocation model. But investors may have it backwards: the “true” volatility of valuation in private equity may be closer to economic reality than the extreme volatility we see in public markets. This has important implications for investors: rather than discounting the attractiveness of private equity by assigning it a higher assumed standard deviation, investors should demand a premium to invest in public equities given its unjustifiably high volatility.

Of course, public equities allow liquidity for investors, but investors are likely overvaluing that feature. Given the extreme volatility of public markets, equities are suitable only as long-term investments and liquidity may not be available or advisable during periods of significant sell-off when it is often most desired.

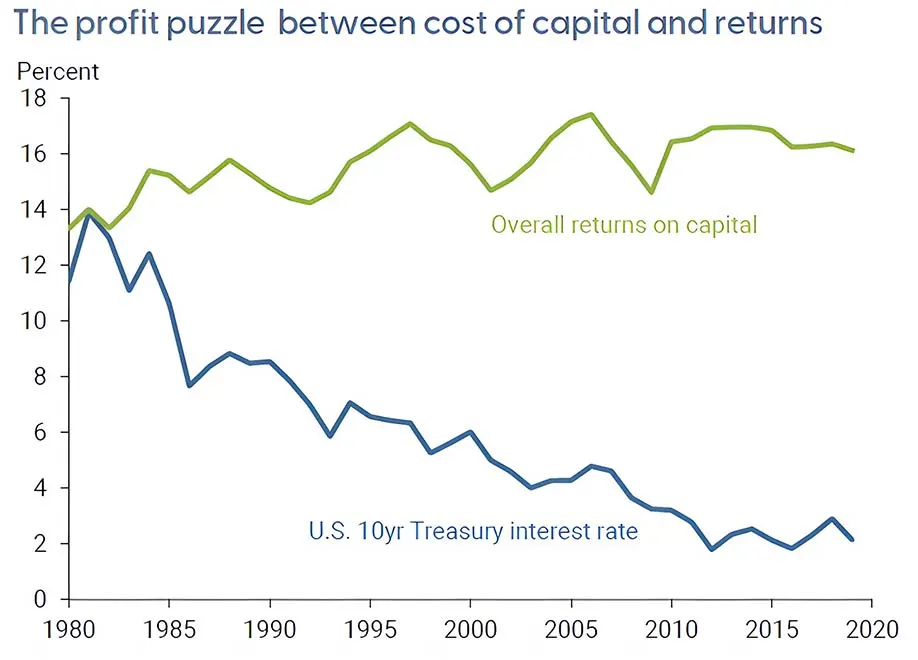

Private equity may be an even more attractive alternative to public equities than it already is. Recent research* has identified a “profit puzzle,” the observation that returns on capital in the economy have remained elevated even as the cost of capital has declined (Chart 8). This is contrary to economic theory that the gap between costs and profits should narrow over time.

* Why Are Overall Profits Outpacing Financing Costs? Anton Bobrov, Carter Davis, Alexandre Sollaci, and James Traina, FRBSF, June 2024.

- Chart 8

-

Returns on Capital and Costs of Capital, 1980-2020

-

-

Source: Federal Reserve Bank of San Francisco

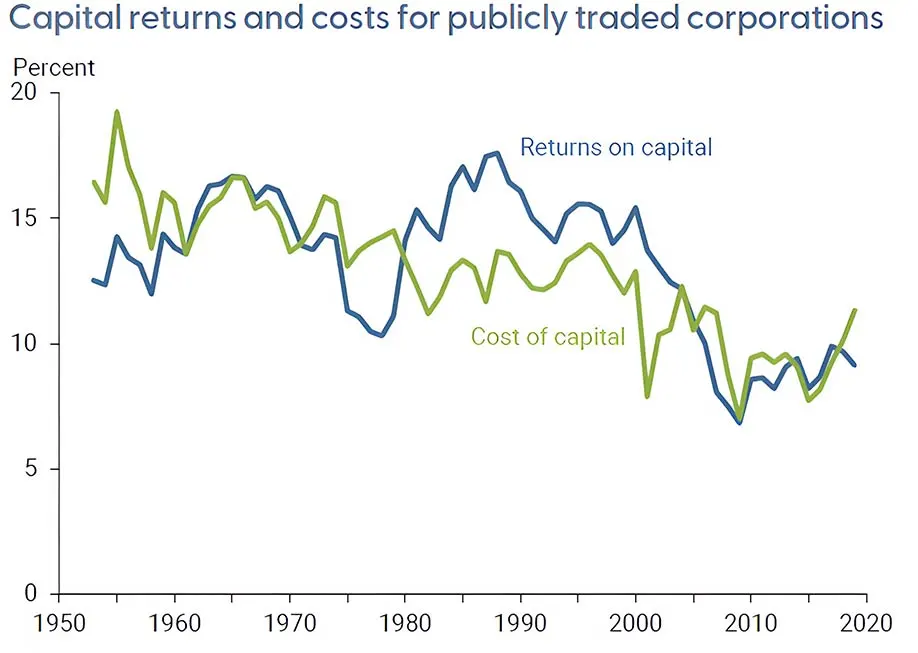

When examining the data of publicly traded companies, the research finds this relationship holds true: returns on capital and costs of capital do, in fact, narrow over time and follow each other closely (Chart 9).

- Chart 9

-

Capital Returns and Costs for Public Companies, 1950-2020

-

-

Source: Federal Reserve Bank of San Francisco

Data on private companies are difficult to observe, but by subtracting the results of public companies from the broader dataset of returns and costs for all companies leads to the conclusion that the “profit puzzle” is explained by the increasing profitability of private companies.

Investors make two big mistakes. By seeking to dampen the very high volatility of equities, investors allocate to hedge funds and bonds, which have generated returns far behind that of equities. Over the past 25 years, US equities have returned 9.1% per annum, hedge funds 6.4% and fixed income 4.2%.* These gaps in performance compound to enormous differences in wealth over time.

The second big mistake is to overvalue the liquidity of the public markets. Liquidity may not be available when it is most needed, in periods of sharp declines, which occur regularly given the extremely high volatility of equities, far greater, again, than can be justified by underlying fundamentals. Overvaluing this liquidity results in under-allocating to private equity, where returns are substantially higher. That excess return of private equity is not due to an “illiquidity premium,” but to the consistently higher profitability of private companies.

Internal combustion engines work by compressing fuel and air and then igniting that mixture with a spark plug. The explosion then pushes the pistons, which generate the power to drive the car. In a smoothly running engine the combustion occurs in a controlled manner, but when the detonations are off, the engine performance is greatly diminished.

In the early days of the automobile, engine “knocking” was commonplace and would cause automobiles to shake violently. Knocking prevented the widespread adoption of automobiles. Billy Durant knew he needed to solve this problem if he was going to sell more cars, and he turned to an engineer at a company he had acquired in 1916, the Dayton Engineering Laboratories Company, Delco, the company that had invented the electric ignition system (which replaced the difficult hand-cranking process) for a solution.

Thomas Midgley joined Delco in 1911 after graduating from Cornell. To determine what was causing engine knock, he built a miniature, high-speed camera to photograph what was happening inside the combustion chamber. His camera revealed that the cylinders were igniting too quickly, causing a surge of pressure.

Midgley experimented with hundreds of chemical additives and eventually settled on tetraethyllead to control the combustion. It worked perfectly. Unfortunately, Midgley developed lead poisoning, which should not have been a surprise since lead was a known hazard for thousands of years. In 1923, General Motors hired the DuPont Corporation to manufacture tetraethyllead and asked Midgley to supervise the project. By the following year, ten people had died of lead poisoning, so General Motors created a new company, the Ethyl Gasoline Company, along with Standard Oil of New Jersey (now ExxonMobil) to manufacture tetraethyllead at its Bayway, New Jersey plant using a different process than DuPont’s. **Five more people died and dozens more were afflicted with hallucinations and insanity.

Still, Midgley pushed forward and determined that the manufacture of “ethyl” as it came to be known was safe. He held a press conference in 1924 where he poured the chemical on his hands and inhaled its vapor for sixty seconds to prove its safety. The State of New Jersey was not persuaded and revoked its manufacturing permit. But in 1926, the federal government overruled the State, demanding that the military required the high-performing lead-based fuel. Soon “ethyl” was added to every gallon of gasoline sold in America. Midgley had to take a leave of absence to recover from lead poisoning, but for General Motors it was a huge success.

* Through 30 June 2024. Benchmarks are Russell 3000 Index for equities, HFRI Fund Weighted Index for hedge funds and the Bloomberg Aggregate Bond Index for fixed income.

** The “bromide process” used by DuPont was replaced with the “ethyl chloride process” by Standard Oil.

When Midgley returned to work, General Motors asked him to solve another problem plaguing its Frigidaire division. In the late 1920s, refrigeration systems utilized different chemical compounds as coolants, including ammonia, chloromethane, propane, sulfur dioxide, among others. These compounds were effective coolants, but were also toxic and combustible, undesirable traits for a household appliance. General Motors asked Midgley to find an alternative refrigerant that was non-toxic and non-flammable.

Midgley eventually settled on combining fluorine into a hydrocarbon. He was confident that the fluorine-carbon bond would be stable and prevent the release of toxic compounds, such as hydrogen fluoride. Midgely and his team were able to synthesize dichlorodifluoromethane, a chemical mouthful to which they gave the more appealing name, “Freon.” It quickly became the standard refrigerant worldwide, and found multiple uses in products such as aerosol containers and asthma inhalers.

Thomas Midgley received every major chemical engineering award. The American Chemical Society awarded him its Nichols Medal in 1923 for the “Use of Anti-Knock Compounds in Motor Fuels.” The Society gave him its highest honor, the Priestley Medal, in 1941. He was named its president in 1944, as well as elected to the National Academy of Sciences.

Lead is one of the most toxic substances on Earth, and this has been known for more than two millennia, identified by the ancient Greeks as the source of insanity and death. Thomas Midgley knew this, and suffered himself from lead poisoning, but its anti-knock properties were too effective to ignore. In 1975, the Environmental Protection Agency began phasing out the use of lead in gasoline, although it wasn’t banned entirely until 1996. Lead poisoning still causes 5 ½ million deaths worldwide, about one-in-ten of all deaths, and more than from car accidents, tuberculosis, HIV/AIDS, suicide and malaria combined.* It imposes a social cost of $6 trillion per year. Lead is one of the most dangerous substances on the planet.

The ozone layer is comprised of three oxygen atoms (O3) and absorbs the Sun’s ultraviolet radiation that would otherwise destroy life on our planet. F. Sherwood Rowland and his postdoctoral fellow Mario Molina at the University of California, Irvine found in the 1970s that chlorofluorocarbons were destroying the ozone layer, thus posing an existential threat to life. In 1987, the world community adopted the Montreal Protocol banning the use of chlorofluorocarbons. In 1995, Rowland and Molina** received the Nobel Prize in Chemistry for their work on atmospheric chemistry in the ozone layer, saving us from certain devastation if not possible extinction.

Of Thomas Midgley’s two important contributions, and colossal blunders, one was a known risk, lead poisoning, and the other (chlorofluorocarbons) an unknown risk at the time. Midgley, General Motors, along with DuPont, Standard Oil and the federal government all knew that lead kills, and that the addition of “ethyl” to gasoline would harm millions. Their actions are inexcusable.

Chlorofluorocarbons were not known as harmful in the 1930s, and while we can’t blame Thomas Midgley for their use, they are a good example of unintended consequences. Solving one problem, engine knocking or finding an effective refrigerant, created far bigger problems. The Germans have a word for this: Verschlimmbesserung, one of their great compound words meaning an attempted improvement that only makes things worse.

Investors continually face both known and unknown risks. By avoiding one type of risk, investors take on other kinds. Seeking to mitigate the extreme volatility of equities leads to accepting lower wealth over time. Overvaluing the illusory liquidity of public markets also results in less wealth to investors by under-allocating to the more profitable private companies.

Thomas Midgley was both the most honored chemical engineer in American history and the source of some of the greatest harm ever done to our planet. His sad denouement is that he contracted polio in 1941 and died in 1944 by strangulation in a contraption he had invented to raise and lower himself from and to bed. Publicly it was deemed an accidental death; privately it was thought to be a suicide.

Investors should think carefully and broadly about the trade-offs of risks they take. Each action has consequences, both known and unknown. Thomas Midgley showed us how the genius to solve one problem could have far-reaching, and devastating, consequences. In other words, verschlimmbesserung.

* https://doi.org/10.1016/S2542-5196(23)00166-3.

** Along with Dutch meteorologist and chemist Paul Crutzen.

-

![Michael Rosen]()

-

Michael A. Rosen

Principal & Chief Investment Officer

Michael Rosen, co-founder and Chief Investment Officer of Angeles Investments, has 37 years of experience as an institutional portfolio manager, investment strategist, and investment consultant.

Please see more insights from Michael Rosen and Angeles here:

www.angelesinvestments.com/insights/home -

July 2024

Connect with us

![Angeles on Linked In]()

Founded in 2001, Angeles is a multi-asset investment firm, building customized portfolios for institutional and private wealth investors.

This report is not an offer to sell or solicitation to buy any security. This is intended for the general information of the clients of Angeles Investment Advisors. It does not consider the investment objectives, financial situation or needs of individual investors. Before acting on any advice or recommendation in this material, a client must consider its suitability and seek professional advice, if necessary. The material contained herein is based on information we believe to be reliable, but we do not represent that it is accurate, and it should not be relied on as such. Opinions expressed are our current opinions as of the date written only, and may change without notification. We, along with any affiliates, officers, directors or employees, may, from time to time, have positions, long or short, in, and buy and sell, any securities or derivatives mentioned herein. No part of this material may be copied or duplicated in any form by any means and may not be redistributed without the consent of Angeles Investment Advisors, LLC.

If you would like, please click this link to receive a copy of our Form ADV Part 2A free of charge. -