-

Investment Insight

4th Quarter 2023 - Storms

Published 01-09-2024-

2023 4th QUARTER QUARTERLY COMMENTARY

-

STORMS

At the end of the 20th century, Americans were asked* to rank the country's greatest achievement in the previous hundred years. Space exploration was, by far, selected as the most substantial American success of the 20th century. Decades after the moon landing, America's triumphs in space remain a significant source of pride, and our astronauts are still venerated as American heroes. Neil Armstrong, the first to walk on the moon, consistently polls** as one of the most important Americans in history.

As heroic as Neil Armstrong was, as all of the astronauts were, the Apollo*** program would literally have never gotten off the ground but for the 20,000 contractors and 400,000 workers who enabled Armstrong**** to reach the moon. The sheer size and complexity of the Apollo program is staggering, but more underappreciated are the intricate engineering solutions that had to be invented from scratch in order to build a rocket capable of sending humans to the moon and to return them to Earth. Among those 400,000 workers, one remarkable engineer took on the most intractable tasks and solved them. Without his energy, determination and brilliance, there would be no moon landing.

* https://www.pewresearch.org/politics/1999/07/03/successes-of-the-20th-century

** https://www.smithsonianmag.com/smithsonianmag/meet-100-most-significant-americans-all-time-180953341

*** The name of the moon-landing program.

**** And Buzz Aldrin and Michael Collins.Prior to the Apollo program, his career was in shambles. The three programs he had led over the previous 15 years were all canceled. But the lessons he learned from those failures enabled him to solve the impenetrable problems presented in the Apollo program.

We learn from experience.* We gain from failure, perhaps even more than from success. Examining how those previous disappointments enabled the eventual success of the space program may help us be better investors as we encounter our own set of hurdles and challenges.

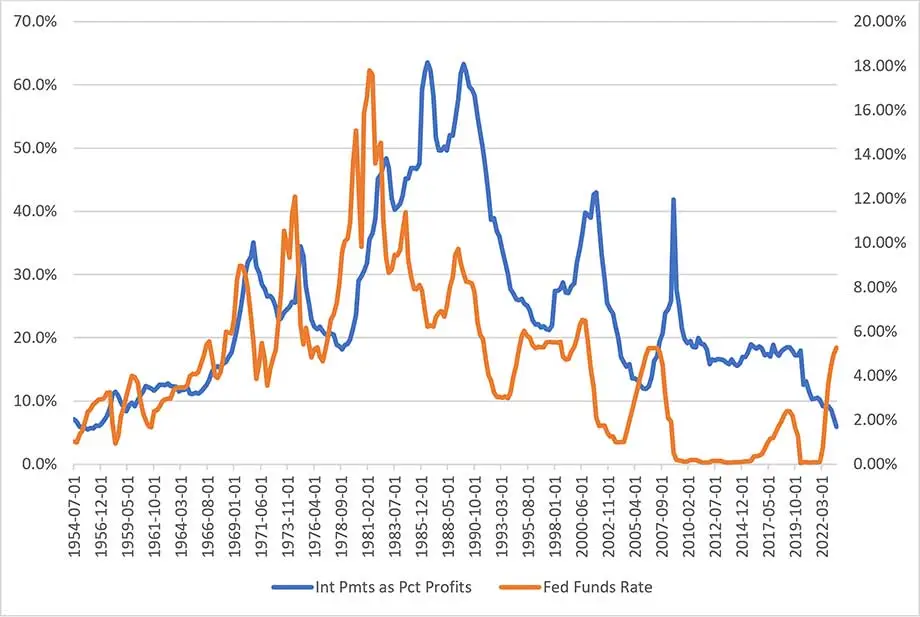

Like the dog that didn't bark,* the big economic surprise of 2023 was the recession that didn't come, despite economists placing high odds at the beginning of the year on a Fed-induced downturn.* Higher interest rates were supposed to raise borrowing costs, a relationship that is seemingly self-evident, but that didn't happen this time. Unusually, net interest payments as a percentage of profits declined last year, even as interest rates were hiked (Chart 1).

* Or we certainly hope to.

** From Arthur Conan Doyle's short story, The Adventure of Silver Blaze, about the disappearance of a racehorse, a mystery solved by Sherlock Holmes. The Scotland Yard detective asks: Is there any other point to which you would wish to draw my attention?

Holmes: To the curious incident of the dog in the night-time.

Detective: The dog did nothing in the night-time.

Holmes: That was the curious incident.

*** Economists surveyed in December 2022 placed 70% odds on a recession in 2023: https://www.bloomberg.com/news/articles/2022-12-20/economists-place-70-chance-for-us-recession-in-2023- Chart 1

-

The Fed Funds Rate & Net Interest Payments as a Percentage of Profits, 1954-2023

-

-

Source: Bureau of Economic Analysis, Federal Reserve System

The key to this puzzlement is profits. Corporations have used profits to de-lever their balance sheets, extend debt maturities and hold record levels of cash. These actions blunted the impact of higher interest rates.

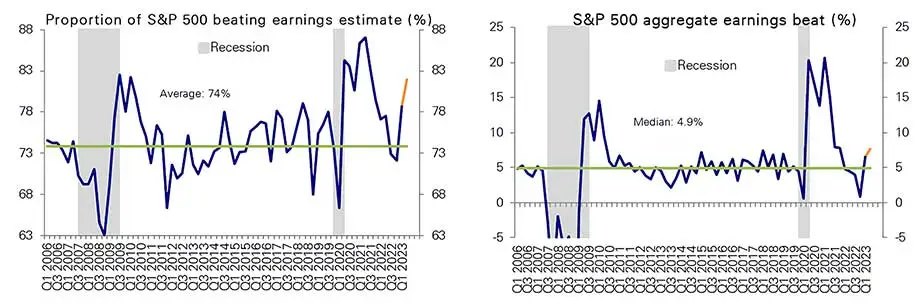

The second, and related, big surprise of 2023 was the strong rally in equity markets, up over 20%.* Profits were behind this rally too, as more companies beat earnings estimates, and by a greater degree, than analysts had expected (Chart 2).

* The MSCI All-Country World Index rose 21.6% in 2023.

- Chart 2

-

Earnings Relative to Estimates, 2006-2023

-

-

Source: Deutsche Bank

Profits drive equities, indeed are the raison d'etre* of equities. The importance of profits to investors cannot be overstated. Changes in tax rates, changes in interest rates, economic growth are all superficial factors affecting equity returns. Profits are what matter to investors.

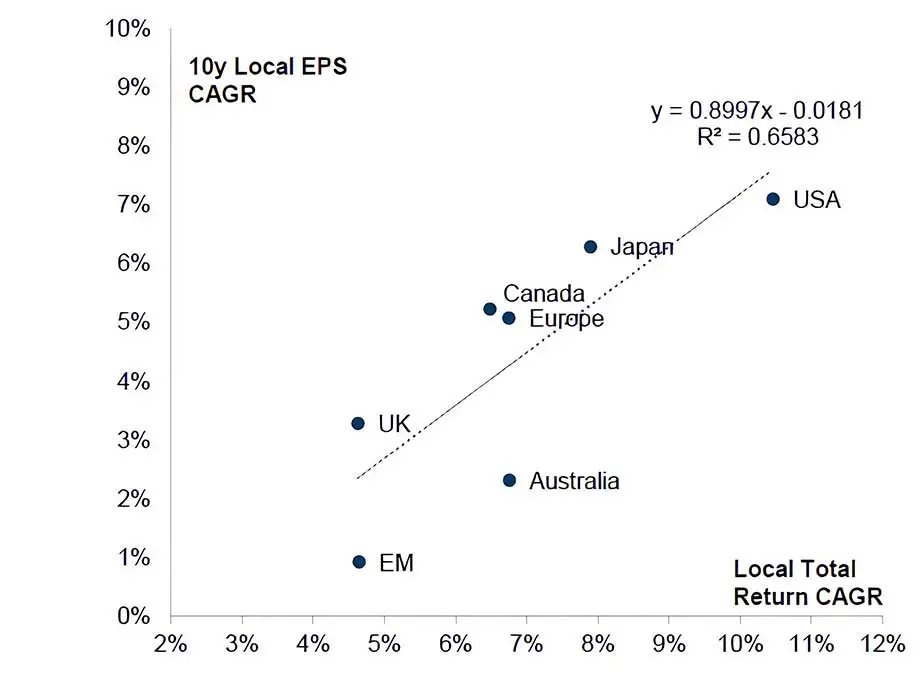

We have discussed before** the outperformance of US equities globally due to the higher profitability of US companies. Indeed, the long-term relationship between earnings growth and equity returns is very close (Chart 3), emphasizing the importance of profits to investment results.

* Reason for being.

** https://www.angelesinvestments.com/insights/investment-insights/4th-quarter-2022-kapitalismus- Chart 3

-

10-Year Annualized Earnings Growth and Equity Returns

-

-

Source: Goldman Sachs

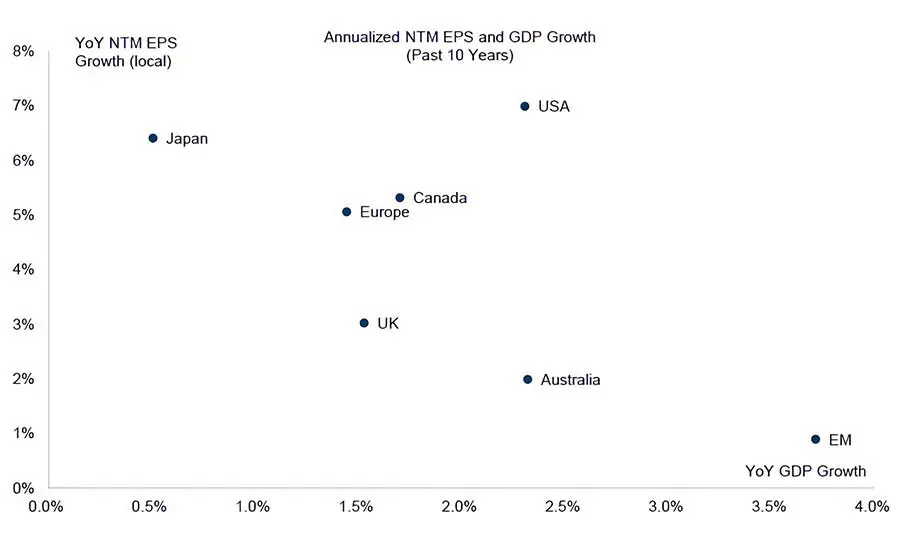

Conversely, the relationship between earnings growth and economic growth is negatively (-0.75) correlated (Chart 4). Owning markets in fast-growing economies is a spurious strategy for investors. Profits are what matter.

- Chart 4

-

Annualized Earnings Growth and GDP Growth

-

-

Source: Goldman Sachs

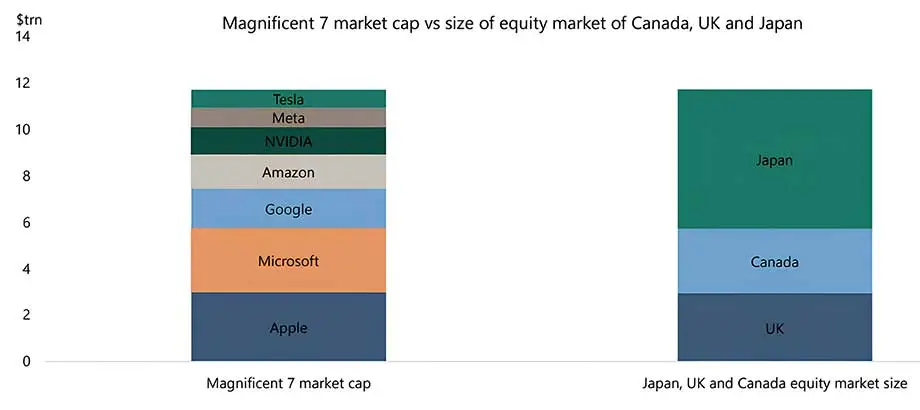

The third surprise of 2023, and the source of much consternation among pundits, is the concentration of market leadership, particularly among the so-called Magnificent 7.* Collectively, this group more than doubled** in value last year, even as 72% of stocks underperformed the broad market. The aggregate capitalization of these seven giants equals the entire equity markets of Japan, Canada and the UK combined (Chart 5).

* Apple, Microsoft, Alphabet, Amazon.com, Nvidia, Meta Platforms and Tesla. References a great movie, and movie score, The Magnificent Seven (1960).

** Up 111%.- Chart 5

-

Market Capitalization of Magnificent 7 vs. Japan, Canada and the UK

-

-

Source: Apollo

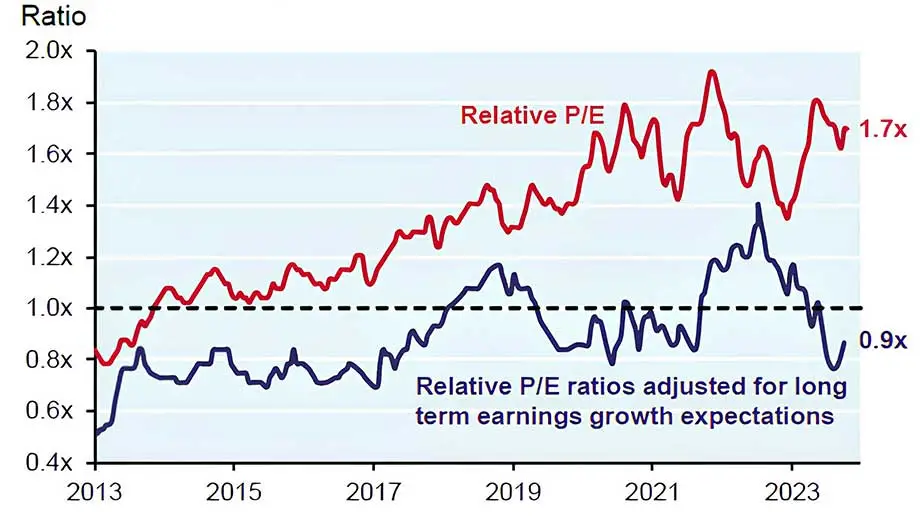

Profits, again, provide the explanation for the strong performance of these companies. For the past decade, these seven have had profit margins that have averaged around 19%, whereas margins for the rest of the market have averaged around 9%. Adjusted for these significantly higher profits, valuations for these leaders may not be so unreasonable (Chart 6).

- Chart 6

-

Valuation of Magnificent 7 Stocks vs. Median Stock, 2014-2023

-

-

Source: J.P. Morgan

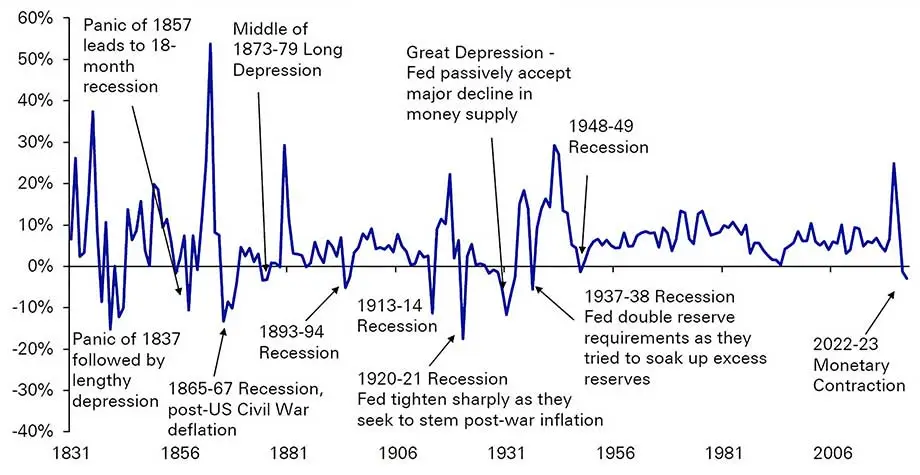

Near-term worries for investors abound, although that is almost always true. Geopolitical tensions are rising, the manufacturing sector is contracting,* and the strong labor market shows signs of softening, both in the decline of temporary workers and in the drop in the hires rate (Chart 7).** The yield curve remains inverted,*** a condition that has preceded each of the last ten recessions.**** Money supply is contracting for the first time in over 70 years, a rare event that historically has been associated with recessions (or worse—Chart 8).

* The ISM PMI Index, a diffusion index, has been below 50 for over a year.

** The number of hires as a percentage of employment.

*** With long-term yields below short-term yields.

**** The inverse is usually, but not always true, that an inverted curve precedes a recession (see 1965).- Chart 7

-

US Hires Rate, 2000-2023

-

-

Source: Bureau of Labor Statistics

- Chart 8

-

Annual Percentage Change in US Money Supply, 1831-2023

-

-

Source: Deutsche Bank

While there are numerous events that could temporarily jolt markets (there always are), investors should be attuned to the far more important systemic shifts occurring in the markets, the economy and the world that have major implications for investment strategy.

The forty-year declines in interest rates and tax rates are over. One can debate about the timing and magnitude, but the future direction of both will likely be higher. Interest rates will rise because inflation is no longer anchored below 2%, and tax rates will be higher because the federal government is running trillion-dollar deficits, spending as much as it did at the peak of the Second World War. The bipartisan embrace of industrial policy* means the government will have a growing role in the economy and an insatiable appetite for revenue.

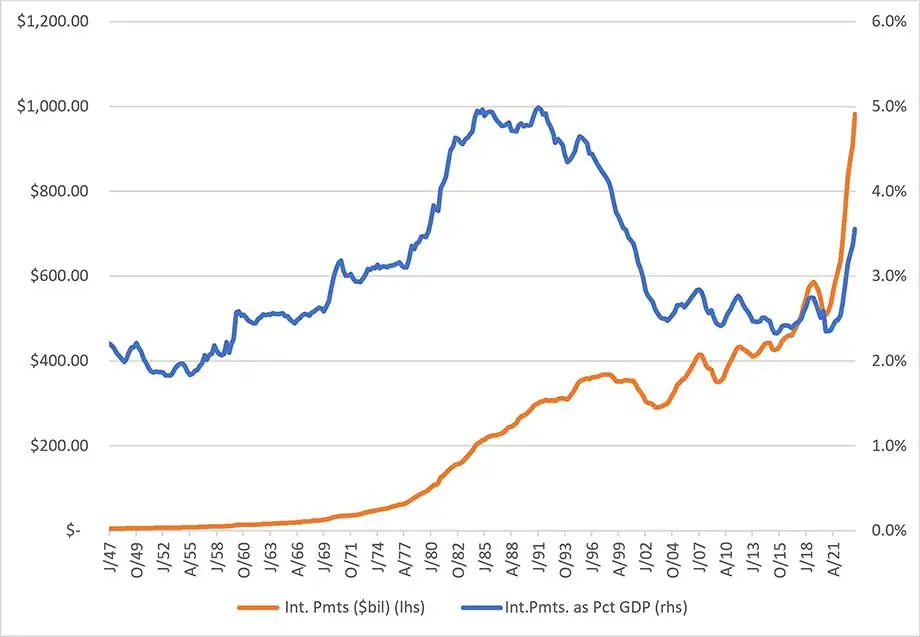

Those deficits have accumulated into the largest debt burden in history, at 100% of GDP, and is projected to climb to 180% of GDP in the next 30 years, according to the (wildly) optimistic Congressional Budget Office.** Interest expense on the debt has already more than doubled in the past year, to nearly $1 trillion annually, greater than the entire defense budget, and the highest as a percentage of GDP in over 20 years (Chart 9).

* Subsidies and trade protection for favored industries.

** https://www.cbo.gov/publication/59233- Chart 9

-

US Government Expenditures and as a Percentage of GDP, 1947-2023

-

-

Source: Bureau of Economic Analysis

Cheap money has moved from abundance to scarcity, with important implications for corporate profits and for investors. Likewise moving from abundance to scarcity is that other critical economic component: labor.

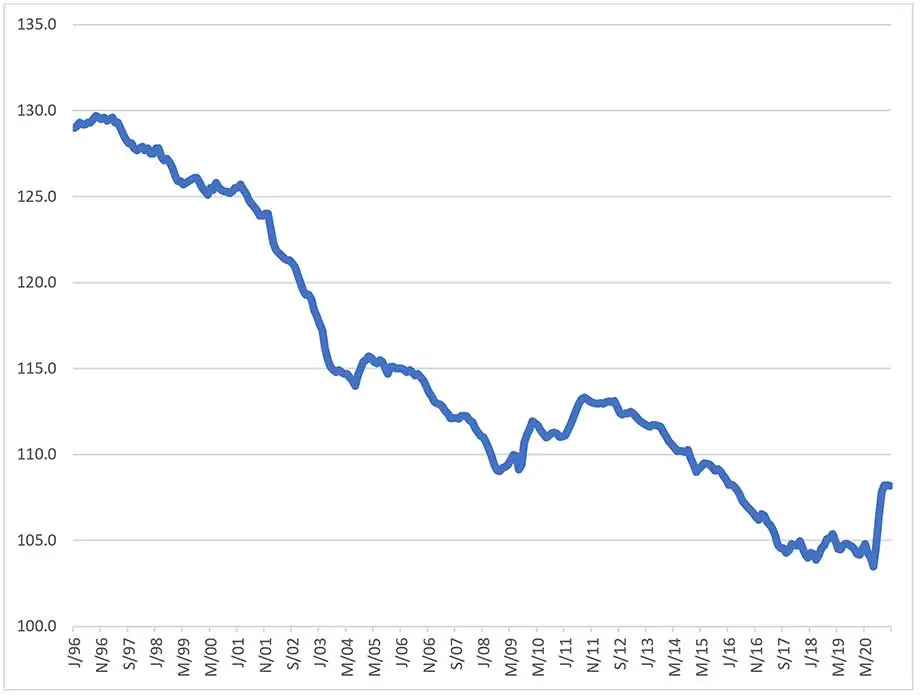

Thirty years ago, there was a one-off, historic shift in the global labor supply curve as more than a billion workers from the previously closed economies of Eastern Europe and China entered the world market. Companies took advantage of this massive labor arbitrage to reduce costs, resulting in both higher profits and lower prices (by 20%) for tradeable goods (Chart 10).

- Chart 10

-

Consumer Price Index for All Urban Consumers: Durables in U.S. City Average, 1996-2020

-

-

Source: Bureau of Labor Statistics

China's working age population peaked in 2015 at 998 million and is projected to fall to 767 million by 2050.* The labor arbitrage is over, and with it the steady decline in prices for tradable goods and the concomitant benefit to corporate earnings.

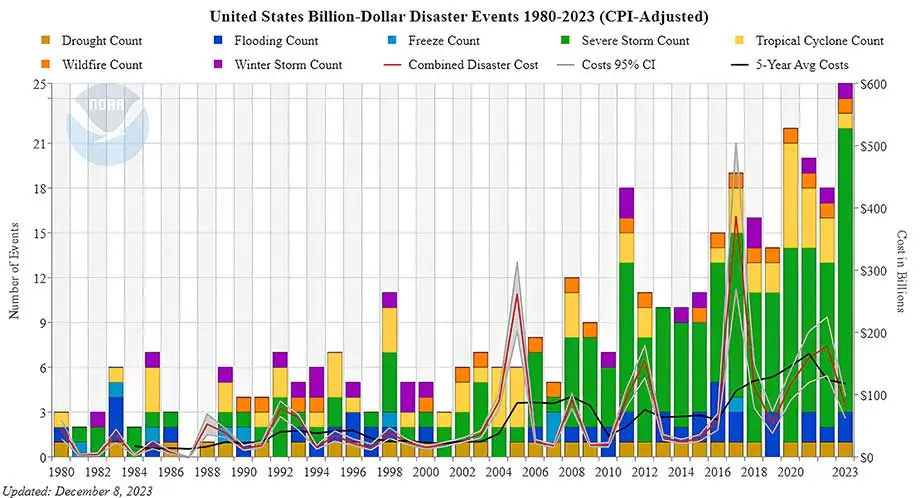

Less clear on the economic implications, but likely to have major impact in the years and decades to come are two additional systemic shifts: climate mitigation and artificial intelligence (AI). Climate damage will cost the United States $600 billion in 2023 (Chart 11), the most on record. Climate mitigation will require massive outlays to develop new technologies and to reconfigure existing infrastructure. Investment in renewable energy already exceeds that in fossil fuels, but the transition is early. There are many long-term benefits to this shift to renewable energy, but there are also short-term costs that should not be overlooked.

- Chart 11

-

Billion-Dollar Disaster Events in the US, 1980-2023

-

-

Source: NOAA

There is much hype, and panic, about artificial intelligence, which is also in its early stages of development and adoption. Its current economic impact is small, but most expect to see modest-to-significant boosts to productivity.* Many jobs, especially in the high-skilled professions, will likely be displaced, although like in all previous technologies, many more opportunities will be created. And as in the case of every previous technological advance, the primary beneficiaries are likely to be those successful adopters rather than the creators of these tools.

Risks and opportunities abound for investors, both in the near-term and in the years to come. This has always been the case. It is also true that risks cannot be avoided; they must be managed. To help us approach managing the risks we face, we turn back to our failed engineer who saved the space program.

North American Aviation had a storied history. Founded in 1928, it was led by James "Dutch" Kindleberger. In the 1930s, it built the T-6 "Texan," the most popular training aircraft in history. The P-51 "Mustang" was developed from sketch to prototype in just 100 days in 1940 and became the most important fighter airplane for the United States air forces. Its B-25 bomber was the most produced American bomber of the war. In all, North American built 42,000 aircraft that helped win the war.

Harrison Storms built model airplanes as a kid at his home in suburban Chicago before graduating from Northwestern at the top of his class with bachelor's and master's degrees in mechanical engineering. He earned a second master's in aeronautical engineering at Caltech, and joined North American Aviation just before Pearl Harbor. After the war, he worked on designing the F-86 Sabre, still the most produced jet fighter in US history, and the F-100 Super Sabre, the first US fighter capable of supersonic flight. In 1957, he was named North American Aviation's chief engineer.

The first project he led was the B-70 bomber, capable of flying at 70,000 feet at a speed of Mach 3.** His critical breakthrough was utilizing compression lift, where the aircraft could ride on its own supersonic shockwave, thereby increasing lift by 30%. He invented a new brazing process to build the honeycombed panels in the fuselage, as well as a new way to roll steel to two-thousandths of an inch. The B-70 was the most capable bomber of its time, but the Air Force canceled it after the prototypes were built and flown.

* See, for example: https://www.mckinsey.com/capabilities/mckinsey-digital/our-insights/the-economic-potential-of-generative-ai-the-next-productivity-frontier#introduction.

** Three times the speed of sound.

B-70

The next project Storms led was the X-15 aircraft for NASA to push the limits of hypersonic flight. It was essentially a manned rocket that flew at altitudes above 50 miles, NASA's boundary of space, qualifying the X-15 pilots for astronaut wings, and achieved a speed of Mach 6.7, 4,520 mph, a record that still stands for manned powered aircraft. The X-15 was made of a new alloy, Inconel-X, and had to be fabricated to tolerances of one-thousandth of an inch. Welding had to be done in an oven at 1900 degrees to even the temperatures on the welds, all of which was new technology Storms invented. After successful flights, NASA canceled the X-15 program.

X-15

North American then won a contract to develop a new intercontinental missile, called the Navaho. It failed on its first eleven launch attempts, and was ultimately scrapped. But it was the first missile to deploy an airborne digital computer and an all-inertial navigation system, and the first to utilize modular (transistorized) circuitry. For the project, North American developed the Chem-Milling process, still used today, to manufacture body panels, and invented new Tungsten arc welding and bonded aluminum honeycomb for the Navaho.

The B-70 bomber, the X-15 aircraft and the Navaho missile were all failures from a corporate perspective. But the techniques that were invented and developed by Storms and his team were essential for future aerospace advances and the ultimate success of the Apollo program.

Navajo Missile

North American separated its rocket division as Rocketdyne, whose engines propelled the Redstone rocket that lifted the Mercury astronauts, and built the massive F-1 engines that powered the enormous Saturn V rocket of the Apollo program.*

* On a personal note, I worked in the San Fernando Valley in the 1990s. My office would shake every time Rocketdyne tested its engines a few miles away.

Storms wanted to build spacecraft, but North American lost the Mercury contract to McDonnell, and the space division of North American was dismantled. Storms convinced Kindleberger to let him rebuild it, and proceeded to raid the rest of the company for its best engineers. One engineer targeted by Storms begged off saying that he needed nine months to finish his Ph.D. Storms assigned a team of engineers to help him and the dissertation was completed the next week. Storms got his engineer.

The Apollo spacecraft and the three stages of the Saturn V rocket were all bid separately. To its surprise, North American won the contract for the spacecraft. The first stage of the Saturn V rocket was simple, just a lot of kerosene that would be quickly discarded after take-off, the third stage was a much smaller component, but the second stage was an engineering nightmare, so Storms bid and won the second stage contract.

The biggest engineering problem was weight. Each pound of payload required 75 pounds of fuel, so weight had to be cut everywhere. The fuel for the second stage was liquid hydrogen, and to reduce weight Storms proposed a common bulkhead to hold both the hydrogen and oxygen rather than having the traditional two separate compartments. The two liquid gases were insulated from each other by a honeycombed structure Storms had used on the B-70.

Storms chose a new aluminum alloy for the body of the rocket, but Stage 2 required half a mile of flawless welds, and the alloy he chose was extremely difficult to weld. Storms created the first sterile welding room, with airlocks to prevent any dust from entering, and invented a new automatic welding machine. Fabricating the bulkhead was a challenge also, as each 20-foot dome had to curve precisely to fit perfectly together. No hydraulic press existed to bend the metal, so Storms found a 60,000-gallon water tank at El Toro Marine Base, sank the sheets in the water and detonated explosives to shape the metal. Somehow it worked.

Storms and his team struggled to meet NASA's timelines and constant changes: in the first three years of the contract NASA made 1,000 changes per month. Meanwhile, Rocketdyne's F-1 engines were failing their tests. Through sheer determination and boundless energy, Storms somehow managed to keep the program on track.

Until January 1967. A catastrophic fire broke out in the Apollo 1 capsule on the launch pad, killing astronauts Gus Grissom, Ed White and Roger Chaffee. NASA's 2,300-page report on the accident did not identify a single cause of the fire, but suggested poor workmanship, pointing the blame on North American.

In fact, NASA was at fault. It insisted, over North American's objections, on using pure oxygen at three times the recommended pressure in the capsule. NASA insisted on an escape hatch that opened inward with a manual release that took 90 seconds to open instead of instantly blowing outward because it was concerned that the explosive bolts might get accidentally triggered. North American had warned against both decisions.

But North American did not want to humiliate its only client, and when NASA demanded that heads had to roll, Harrison Storms was fired. The 35,000 employees at North American were in tears when they heard the news. Storms worked as a consultant to the industry for a few more years, and died in obscurity in 1992.

Harrison Storms transformed the aerospace industry. His innovations in design and manufacturing more than 60 years ago are foundational elements today, his achievements as remarkable to us as they were in his time. He received no ticker-tape parade, but his contributions to the Apollo program were far more consequential than the men he sent to the moon.

We face our own serious challenges today. Political polarization that rips at the social fabric of our country; geopolitical tensions and actual wars that have killed, injured and displaced millions; an economic backdrop of debt and inflation that we haven't seen in more than a generation.

But we shouldn't forget some of the remarkable breakthroughs we saw in just the past year. We have a new class of drugs, GLP-1,* developed to treat Type 2 diabetes, but now proven effective in combatting obesity and even depression. There were advances in the development of nuclear fusion, a clean, inexhaustible cheap fuel. A cure was found for sickle cell disease, a debilitating and sometimes fatal illness affecting 40,000 Americans. Artificial intelligence was able to translate brain patterns into words, promising to liberate the thoughts of those who have lost their speech. And the most downloaded app of 2023, ChatGPT, is already diagnosing complex medical problems.

Harrison Storms met every engineering challenge with determination and inventiveness, creating new solutions when ones didn't exist. His early career failures were anything but, as the tools he developed on those projects would be used to solve the many future difficulties in the Apollo program.

We have had many successes, and we face many challenges. The determination and innovation that Harrison Storms exhibited, through canceled projects, soaring successes and a final, undeserved ignominy, is required of us today. We give him the final word:

"We need to work with thoughtful courage and not be blinded by fearful safety."

A message for us all.

* Glucagon-like peptide-1.

-

![Michael Rosen]()

-

Michael A. Rosen

Principal & Chief Investment Officer

Michael Rosen, co-founder and Chief Investment Officer of Angeles Investments, has 37 years of experience as an institutional portfolio manager, investment strategist, and investment consultant.

Please see more insights from Michael Rosen and Angeles here:

www.angelesinvestments.com/insights/home -

January 2024

Connect with us

![Angeles on Linked In]()

Founded in 2001, Angeles is a multi-asset investment firm, building customized portfolios for institutional and private wealth investors.

This report is not an offer to sell or solicitation to buy any security. This is intended for the general information of the clients of Angeles Investment Advisors. It does not consider the investment objectives, financial situation or needs of individual investors. Before acting on any advice or recommendation in this material, a client must consider its suitability and seek professional advice, if necessary. The material contained herein is based on information we believe to be reliable, but we do not represent that it is accurate, and it should not be relied on as such. Opinions expressed are our current opinions as of the date written only, and may change without notification. We, along with any affiliates, officers, directors or employees, may, from time to time, have positions, long or short, in, and buy and sell, any securities or derivatives mentioned herein. No part of this material may be copied or duplicated in any form by any means and may not be redistributed without the consent of Angeles Investment Advisors, LLC.

If you would like, please click this link to receive a copy of our Form ADV Part 2A free of charge. -