-

-

![Michael Rosen]()

-

CIO Insights are written by Angeles' CIO Michael Rosen

Michael has more than 35 years experience as an institutional portfolio manager, investment strategist, trader and academic.

RSS: CIO Blog | All Media

O Pais do Futuro

Published: 11-30-2015Charles de Gaulle (photo below)—imperious, disdainful, utterly French (and venerated for it in France)—noted 50 years ago that “Brazil was the country of the future.” With more than 200 million people and encompassing nearly 3.3 million square miles (about the size of the United States), Brazil is the fifth largest country in the world by population and area, and the 9th largest economy. It would seem that the future for Brazil has arrived.

Unfortunately, it is more like back to the future. Brazil is in the midst of a classic balance of payments problem. It’s growth in the past decade had been fueled by foreign capital and rising prices for its principal commodities: soy, wheat, and especially, iron ore. It was a happy, self-reinforcing cycle of strength.

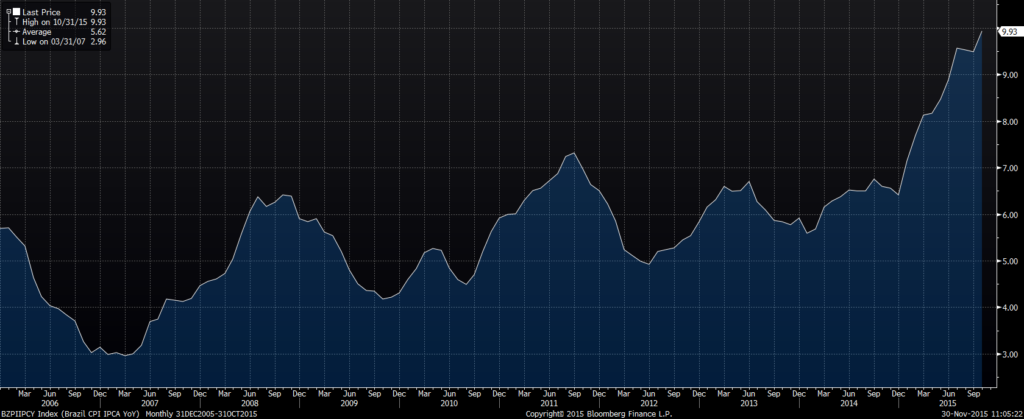

Now, with commodity prices plunging and foreign capital withdrawing, it’s an unhappy spiral down. Real GDP will fall 3% this year, the real is off 20% and inflation is 10% (and rising—see chart below, past 10years). The government is attempting to spend its way out of this hole, running a budget deficit of 7% of GDP, the current account is also in deficit (4% of GDP), and the 5-year government bond yields more than 15%. The Bovespa (stock market) is off 45% over the past year. Its economic heft notwithstanding, the average Brazilian is not especially well-off, as per capita GDP ranks about 74th in the world (IMF), ahead of Libya but behind Suriname.

All this describes the classic balance of payments crisis. The bad news is that it generally does not end without a lender of last resort (usually the IMF) stepping in and imposing massive austerity measures to slash the budget and choke off inflation. This then causes a large contraction in the economy and a drop in the currency, leaving the country poorer, although (in theory) in a better position to resume economic growth.

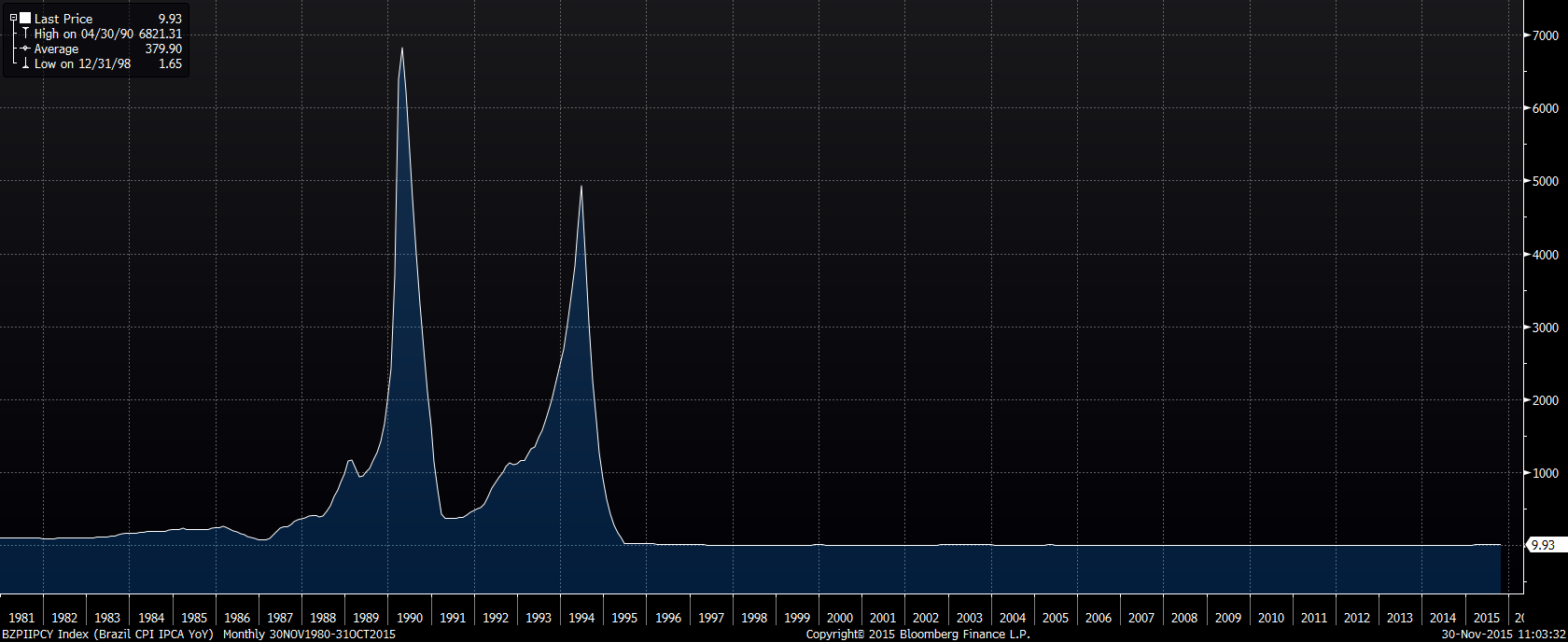

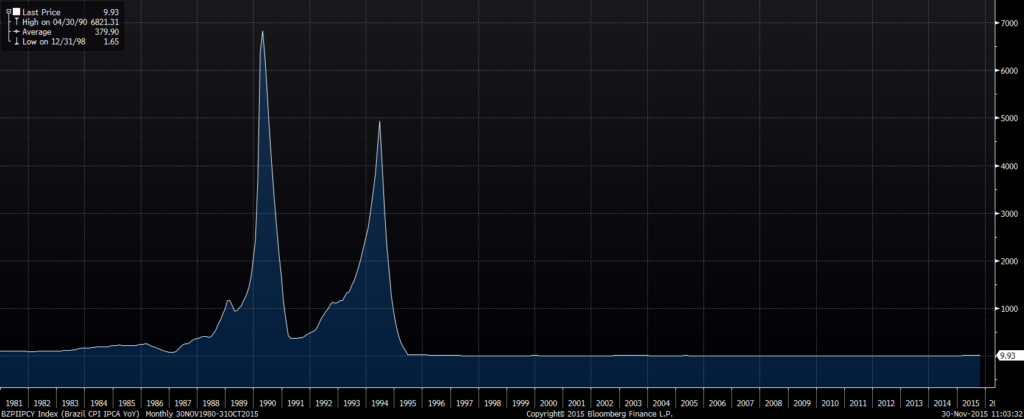

Many things compound the challenges for Brazil: one unique aspect is that the majority of domestic lending and wages is linked to inflation, a relic of past inflationary crises. 60% of Brazil’s workers are covered by collective bargaining agreements, for example, which contain automatic inflation escalators. Brazil is a long way from the 6,000% inflation it had 25 years ago (graph below), but inflation is likely to move higher before it will be addressed. But anyone who lived through the hyper-inflation of that period (I was there to see prices in the stores change daily) is right to be fearful.

Less unique to Brazil, but equally challenging, is the political mess. A Marxist union leader, “Lula” da Silva, came to power in 2003 and had the good fortune of seeing commodity prices rise ten-fold during his reign, and the good sense to leave in 2011. His successor, Dilma Rousseff, who actually fought as a Marxist guerrilla, has not been so lucky. And neither one of them changed the pervasive corruption of the country’s political, economic and social fabric. The results are in evidence today.

So back to de Gaulle. He was right to call Brazil the country of the future. But the full quote is more apt: Brazil is the country of the future…and always will be.

Print this Article-

![AprÃs moi le déluge]() 5 Jan, 2016

5 Jan, 2016AprÃs moi le déluge

In more ways than one.We greeted the new year with an actual deluge, at least here in California, as the long-promised ...

-

![Fireside Reading]() 1 Mar, 2024

1 Mar, 2024Fireside Reading

Seven new selections for you - 3 fiction, 4 nonfiction - while it's still fireside reading season. Enjoy! ...

-

![Mismatch]() 20 Mar, 2023

20 Mar, 2023Mismatch

Bankers have always had a bad rap. Cicero, writing in De Officiis in 44 BCE, referenced Cato the Elder, the great Roman ...

-