Trade

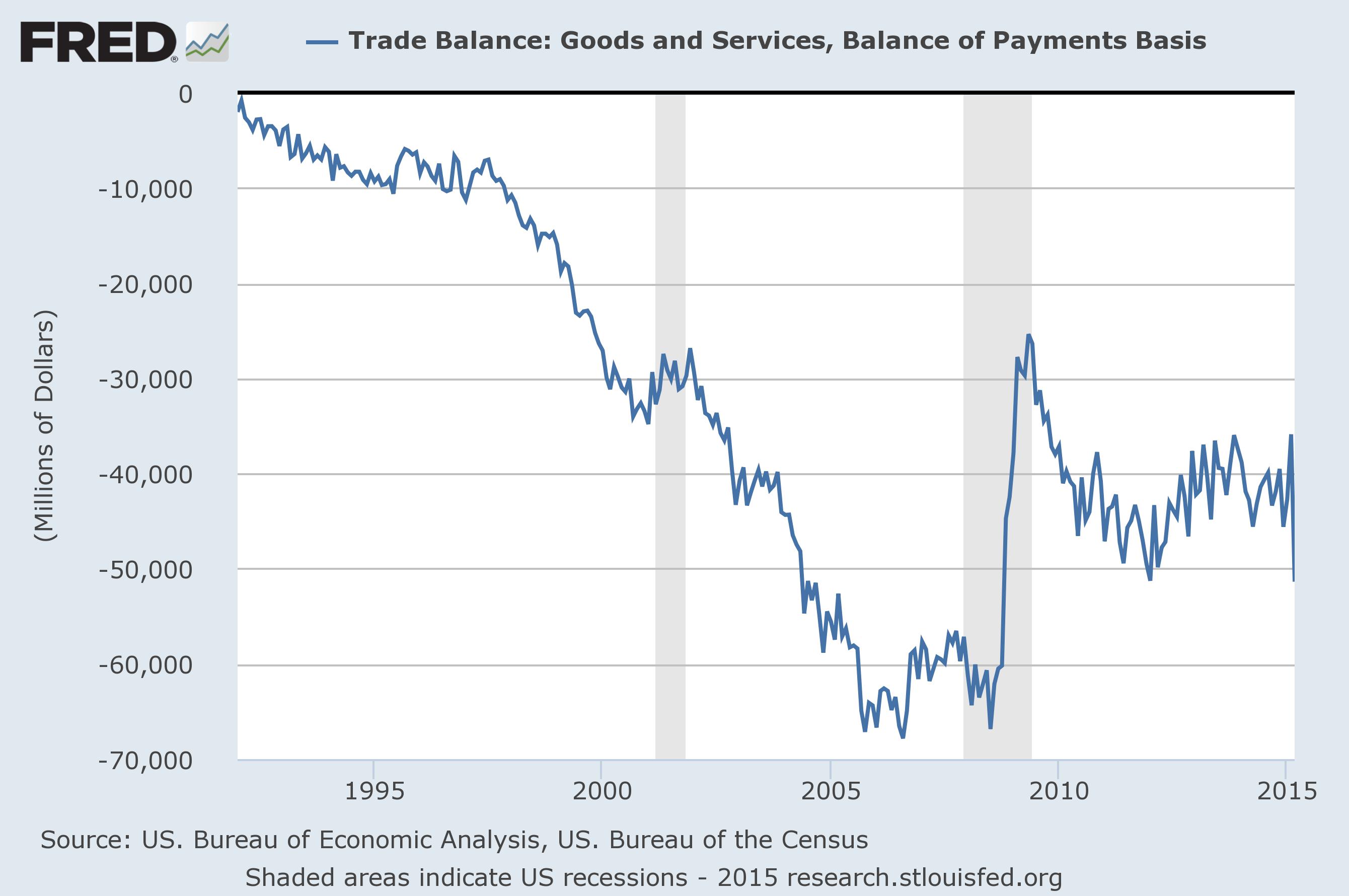

The trade deficit ballooned in March to over $51 billion, $8.6 billion more than a year ago. Exports were up a little, but imports surged, up more than $17 billion from February, the biggest monthly rise in imports since 1992. Over the past year, imports are up 1% while exports are down more than 3%.

Some of the surge in imports can be attributed to the end of West Coast port strikes, which released a flood of imports (mostly cars and cell phones) into the US. While it makes sense that we should see a spike in imports, we should have also seen a jump in exports, but we didn’t, raising questions about the competitiveness of US products.

Why do we care? Well, one immediate impact will be seen in the 1st quarter GDP revision, from +0.2% to a negative number (probably around -0.5%). So the economy contracted in the 1st quarter, but another way of looking at the trade deficit is that it highlights the relative strength of the US economy: booming imports are indicative of strong demand for goods.

I still think the weakness in the 1st quarter will fade into modest growth for the rest of the year. As I emphasized in my quarterly letter (Funambulism), the biggest near-term hurdles to growth are supply-side—capital investments and labor force growth—not insufficient demand incentives. We’ll come back to this topic again, no doubt.