Distortion or Reflation?

A month ago, Germany could borrow for 10 years at a rate of 0.06%. Lenders were also happy that day to earn 0.47% for the next 30 years. That’s $4,700 of annual interest for every $1 million. Investors were happy with this yield because the ECB was buying up all the newly issued bunds, deflation was omnipresent, and, well, Germany is a good credit.

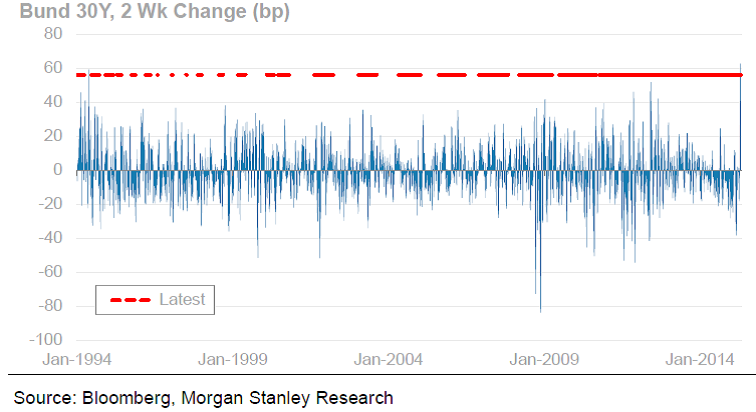

Their happiness didn’t last long, as rates jumped 70 basis points over the subsequent two weeks, wiping 0ut about 30 years of income.

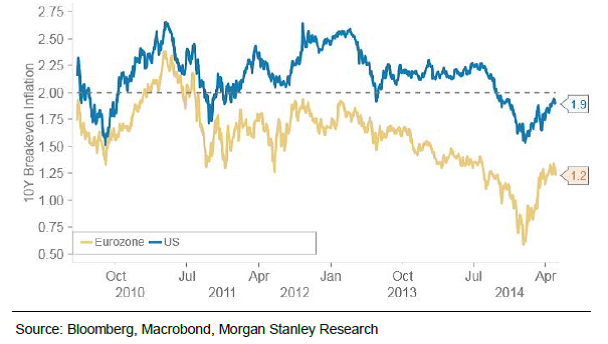

It’s logical to blame central bank meddling in the bond markets for these gyrations, but the market may also be saying that inflation may not be as dormant as suggested by these low yields. Indeed, the surge in government bond yields coincided with a notable rise in inflation expectations: by 20 basis points in the US, 45 basis points in Europe.

I don’t (never did) subscribe to the hyper-inflation scare of massively expanding central bank balance sheets, and I also think sub-1% inflation for decades to come puts too much weight on the end of economic growth and the ineffectiveness of monetary policy. Powerful deflationary forces remain, debt and demographics most prominently. And I expect central banks to continue to distort markets. But growth and inflation will (one day) return, and long-term investors are likely to be happier with a balanced portfolio of equities than the investors who lent 30 years at 0.47%.